Build vs Buy Accounting Software: The 2026 Line

Build vs buy accounting software in 2026: when to fire QuickBooks, sales-tax SaaS, and payroll, and when keeping them is the smart call.

By Mike Hodgen

The blanket advice everyone repeats is wrong half the time

If you've ever asked anyone whether you should build vs buy accounting software, you got the same answer. Never build accounting. Never build payroll. Never touch tax. Buy QuickBooks, buy Avalara, buy Gusto, and move on with your life.

That advice is right often enough that people stop thinking. And that's the problem.

It's a slogan, not a decision rule. It's correct in enough cases that it sounds like wisdom, but it quietly leaves money and control on the table in the cases where it's wrong. I know because I drew a sharper line, and I drew it by actually replacing three of these tools. Not in a strategy deck. In production, across a company I run and an e-commerce brand I operate in San Diego.

Here's what I learned: the line in 2026 is sharper than most people realize, and it's not the line they tell you. The advice to "never build" assumes the only variable is risk. It ignores pricing that scales against you, data you don't own, and vendors who can ban you from using your own numbers however you want.

So I'm not going to hand you a slogan. I'm going to hand you a rule you can apply to your own finance stack this quarter.

We're going to walk through three categories: cloud accounting (the ledger), sales-tax compliance, and payroll. Each one sits at a different point on the build-versus-buy line, and once you see why, the decision stops being a guess.

The real rule: own the ledger and the logic, rent the regulated rails

Here's the rule, stated plainly so you can steal it:

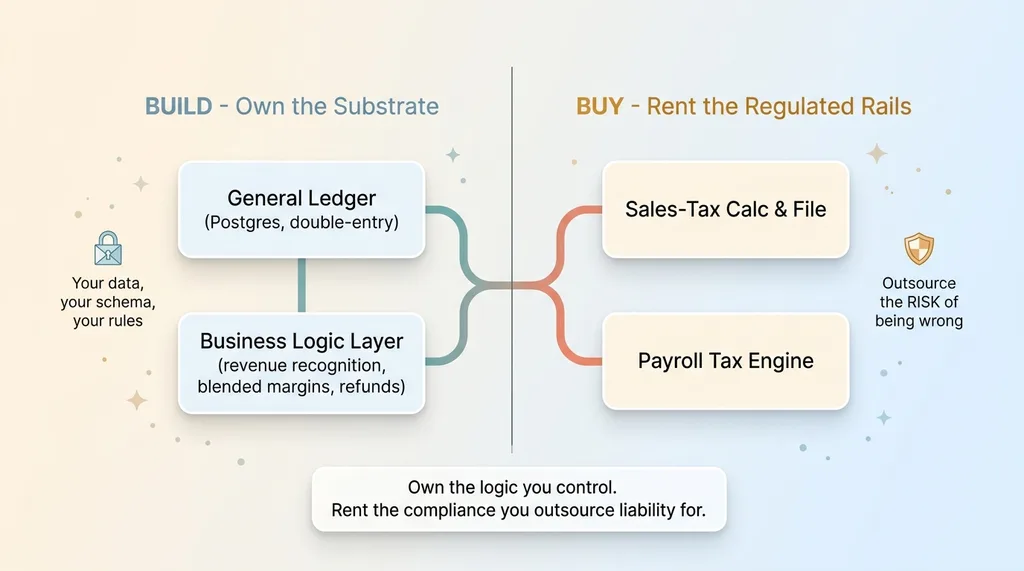

The build vs buy rule: own the substrate, rent the regulated rails

The build vs buy rule: own the substrate, rent the regulated rails

Build the general ledger and the business-logic layer in-house on primitives you own. Keep buying anything where a mistake is a direct regulatory penalty, until you can prove your build to the cent.

That's it. Two halves. Own the substrate, rent the regulated rails.

What 'owning the substrate' actually means

The substrate is your ledger and your orchestration layer. It's where your financial data lives and where your competitive logic runs. There is no good reason to rent those.

When you rent them, your numbers live in someone else's database schema, behind an API you don't control, governed by terms you didn't write. Your custom revenue recognition, your blended margin views, your weird-but-correct way of handling refunds, all of that gets bent to fit a tool instead of the other way around.

The substrate is yours. Build it. This is the pay for primitives, build the logic approach applied to finance: you buy the boring, hard, commoditized inputs and you build the part that's actually your business.

Why regulated rails are different

The other half is the regulated rails: the calc-and-file machinery for taxes and payroll. Here a mistake isn't a bug you patch on Tuesday. It's a fine. It's a penalty notice. It's an employee whose withholding was wrong.

So you outsource the risk of being wrong, not just the work. You keep paying a vendor to be liable for accuracy until you can prove, with tests and historical replay, that your own engine produces the exact same numbers.

"Logic you control" and "compliance you outsource the risk of" are two different things. The blanket advice treats them as one. That's the whole mistake.

Fire the ledger first: why QuickBooks is the easy call

If you're going to replace QuickBooks with a custom finance stack, the ledger is where you start. It's the easiest call you'll make.

A double-entry ledger is solved, owned plumbing

A double-entry ledger is not a frontier problem. It's 500-year-old accounting wired into a database. Debits equal credits, entries never half-post, the books always balance. The rules haven't changed since the Medici.

That maturity is exactly why it's safe to own. The surface area is stable. You're not chasing a moving target.

I replaced a QuickBooks ledger with an owned Postgres ledger built on triggers that physically cannot half-post. The database itself enforces that every transaction balances before it commits. It's provable, it's testable, and it's mine.

What you get back: your data and your rules

Two things change the day you own the ledger.

First, your financial data stops living in someone else's schema behind an API you don't control. You can query it directly. You can join it against inventory, against ad spend, against anything. This is what "own your data accounting" actually buys you.

Second, you encode your own business logic instead of bending to the tool. My DTC brand has revenue recognition quirks that no off-the-shelf chart of accounts handles cleanly. In an owned ledger, I just write them.

The honest tradeoff: you own reconciliation now. You own the edge cases. You write the tests that QuickBooks wrote for you. That's real work.

But the surface area is stable, so you pay that cost once and it stays paid. That's why the ledger is the first thing to fire, not the last.

The first trigger to pull: per-filing SaaS that scales with your footprint

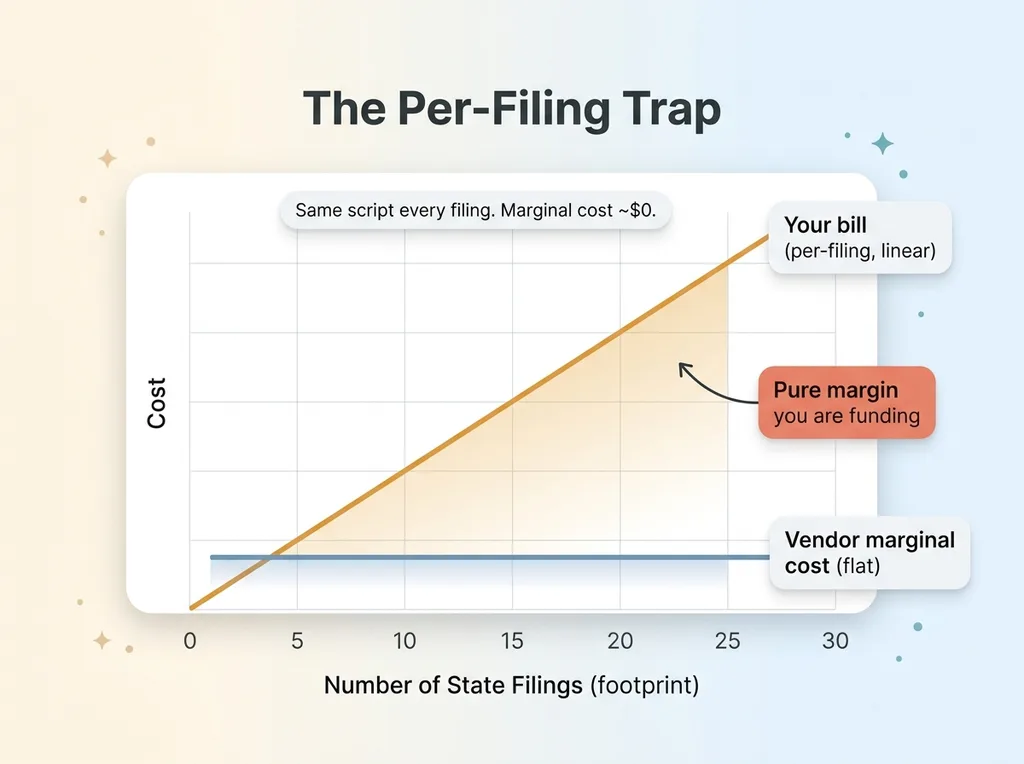

The cleanest signal that it's time to build isn't principle. It's pricing.

Why unit economics, not principle, decides

Watch how a vendor charges you. If the bill scales with the value you get, fine, keep paying. If it scales with your footprint, with something you could automate once, the math is about to flip on you.

Pricing asymmetry: flat vendor cost vs linear customer cost on per-filing SaaS

Pricing asymmetry: flat vendor cost vs linear customer cost on per-filing SaaS

A sales-tax SaaS that charges per filing is the textbook case. Open a new state nexus, and your bill goes up. Open ten, it goes up ten times. But the underlying work, generating a return and submitting it to a portal, is the same script every time. You're paying linearly for something that costs the vendor almost nothing at the margin.

I ran the math behind replacing SaaS with software you own, and the per-filing model is where it breaks fastest. The vendor's cost is flat. Your cost is linear. The gap is pure margin you're funding.

Sales-tax compliance as the textbook case

So I killed a per-filing sales-tax provider and replaced the filing automation with an owned script that talks to the state portals directly. The script doesn't care if I'm registered in three states or thirty. The marginal cost of one more filing is zero.

One important caveat, because this is where people overbuild. The tax rates and rules are the genuinely hard part. Rates change, boundaries shift, product taxability is a swamp. If a vendor sells accurate rate data cheaply, keep buying that. Build only the filing and orchestration around it.

That's the pattern again: buy the hard, commoditized input (rate data), build the part that's just automation you'd otherwise rent forever (the filing).

Payroll: the case you build last, and only behind proof

Payroll is where I'm most conservative, and you should be too.

Why payroll stays bought longer

A payroll mistake is two failures at once: a regulatory penalty and an angry employee. Get withholding wrong and you've got a tax problem and a trust problem walking into your office on Friday.

So payroll stays bought longer than anything else in the stack. The risk-to-reward on a sloppy build is terrible. This is the regulated rail in its purest form, and the default answer is keep paying the vendor who's liable for accuracy.

I kept a payroll product running long after I'd replaced the ledger and the tax filing. Not because I couldn't build it. Because I hadn't yet earned the right to.

When the line moves: 170+ tests and a penny-perfect replay

The line moves only when you can prove your build, not when you think it's ready.

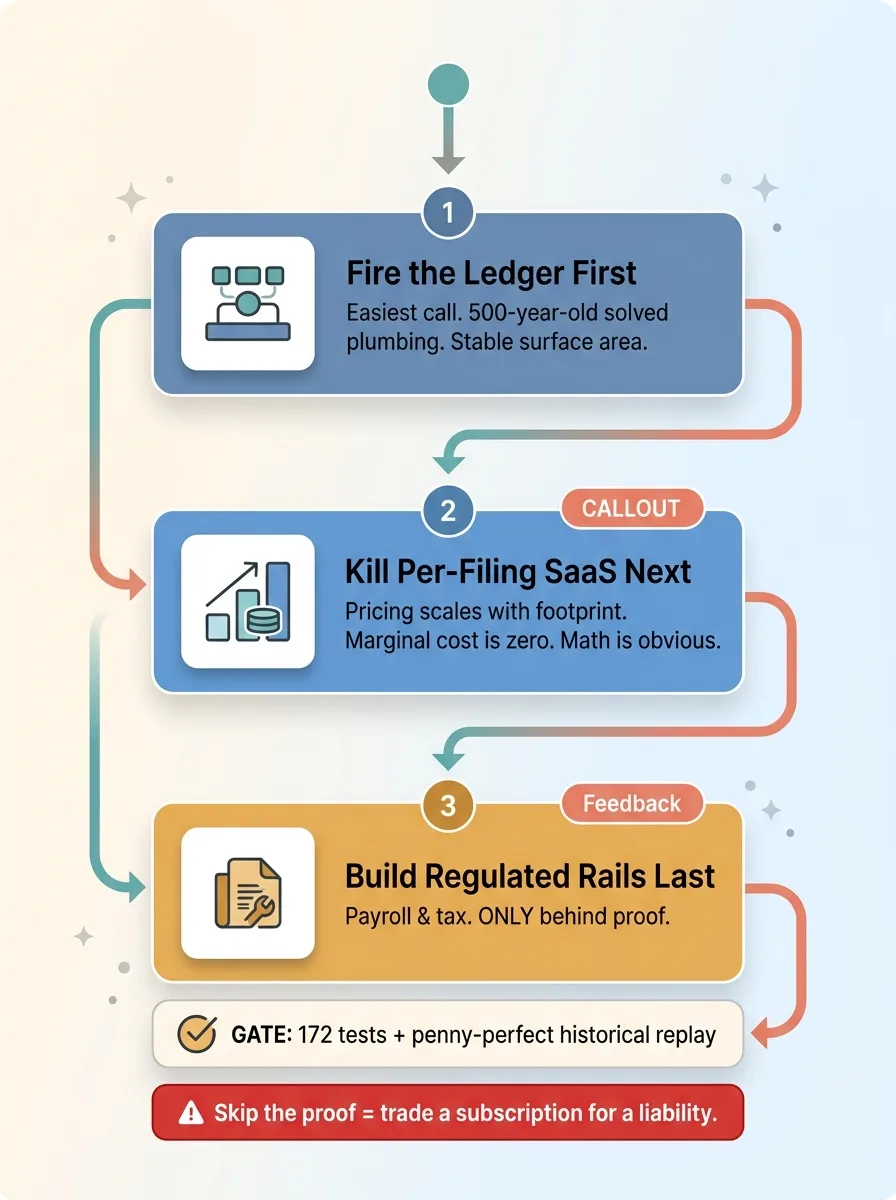

Build order sequence: ledger first, per-filing SaaS next, regulated rails last behind proof

Build order sequence: ledger first, per-filing SaaS next, regulated rails last behind proof

I eventually built a payroll tax engine behind 172 tests, but the tests weren't the standard. The replay was. I ran the new engine against real historical payroll data and confirmed it produced the exact same numbers as the tool it replaced. To the cent. Across actual pay periods that had already been filed and accepted.

That's the bar. You don't ship a payroll engine you believe is correct. You ship one that reproduces known-good results penny-for-penny on real data, and fails loudly when it doesn't.

This rule generalizes to every regulated rail. Build it only after you can replay and verify against the system it replaces. Never on faith. The day your custom engine matches the old one to the cent across a year of history is the day you've earned the switch.

Xero's 2026 API repricing is why owning the substrate matters

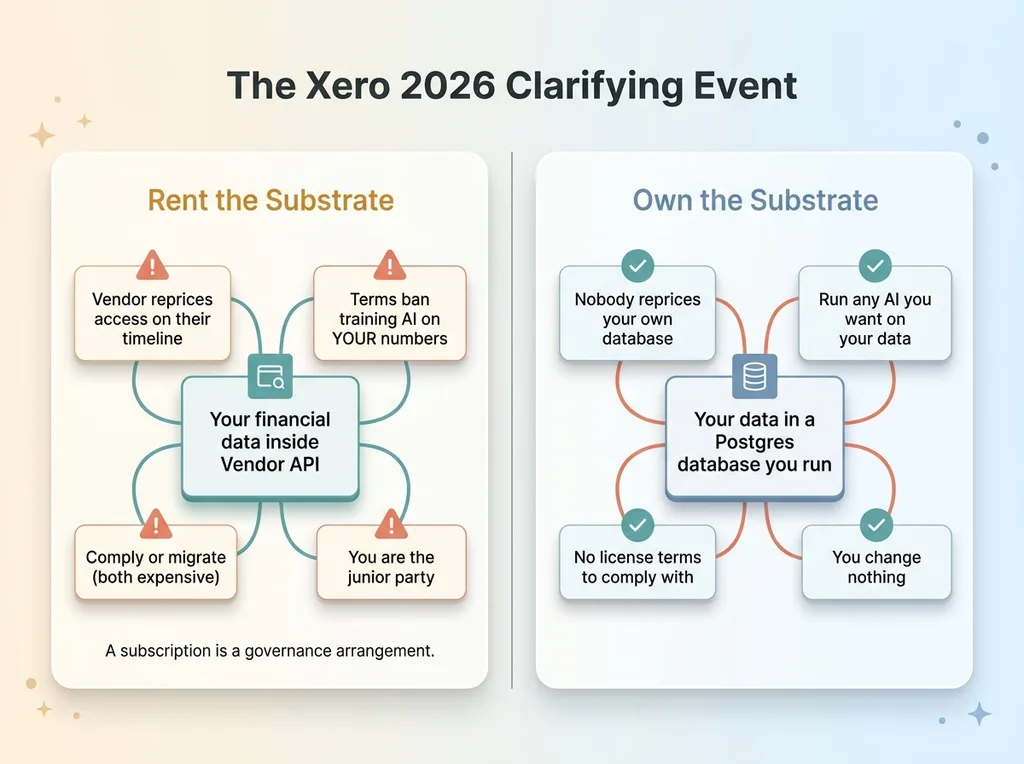

If you need a reason to take "own the substrate" seriously, look at what just happened with Xero.

Vendor lock-in as a governance arrangement (Xero 2026 API repricing)

Vendor lock-in as a governance arrangement (Xero 2026 API repricing)

For 2026, Xero repriced API access and added terms prohibiting using the data to train AI. Sit with that for a second. Your financial data, your transactions, your customers, and the vendor gets to decide whether you're allowed to run AI on it.

This is the live risk the "never build" crowd ignores. When your finance data and workflows live inside a vendor's API, that vendor can reprice access on their timeline. They can restrict what you do with your own numbers. They can change the terms whenever it suits their roadmap, and your only options are comply or migrate, both expensive.

You're not just paying a subscription. You're accepting that someone else governs your financial nervous system. They decide what's allowed, what costs more next year, and whether the AI workflows you've built on top of your own data are permitted to exist.

That's the asymmetry. A subscription feels like a cost line. It's actually a governance arrangement where you're the junior party.

Owning the ledger and orchestration removes that leverage from the relationship entirely. Nobody reprices access to a Postgres database you run. Nobody bans you from training AI on data that sits in your own schema. The Xero change isn't an outrage so much as a clarifying event: it shows you exactly what you signed up for when you let a vendor hold the substrate.

This is what "own your data accounting" means in practice. Not a slogan. The difference between a vendor changing your terms and you changing nothing at all.

How to draw the line for your own finance stack

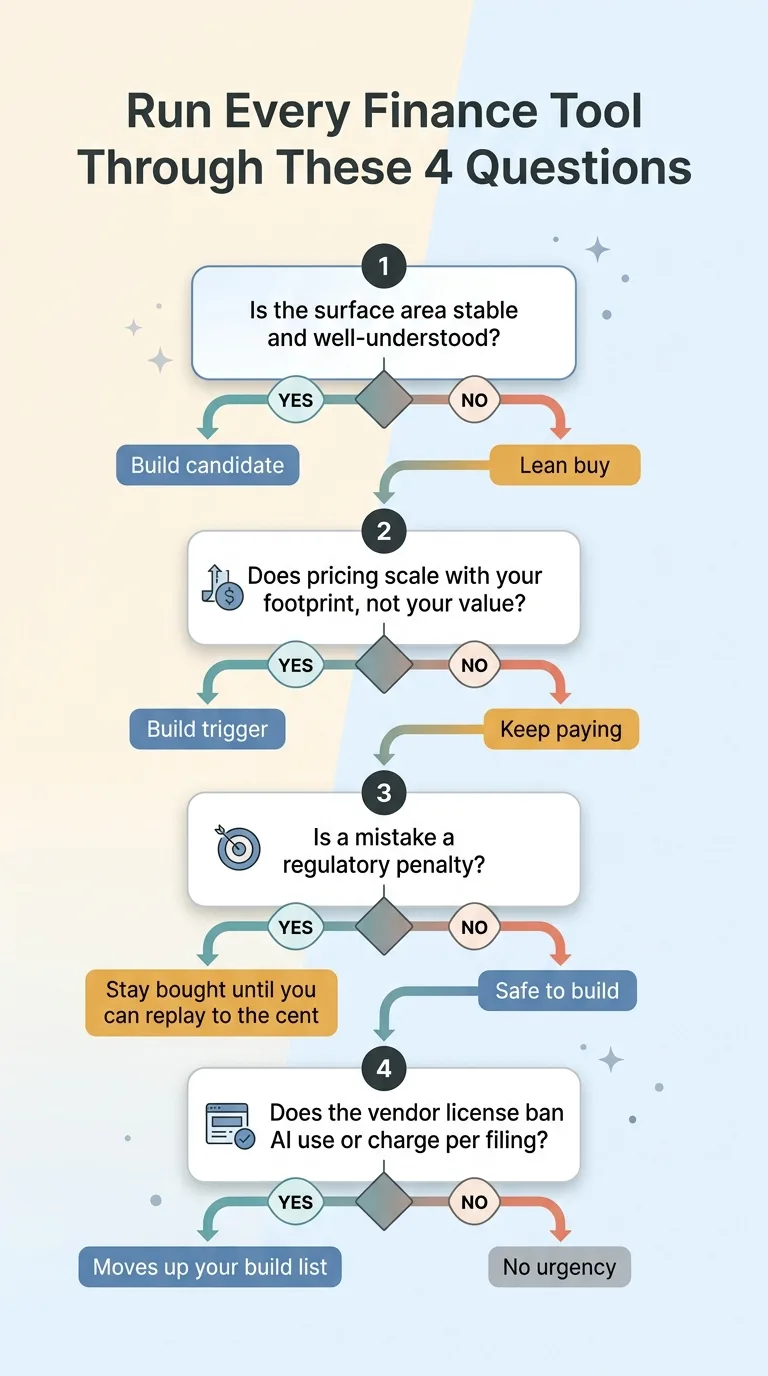

Here's the checklist. Run each tool in your finance stack through these four questions.

The four-question decision checklist for build vs buy

The four-question decision checklist for build vs buy

1. Is the surface area stable and well-understood? A double-entry ledger hasn't changed in centuries. If the problem is mature and boring, it's a build candidate. If it's a fast-moving compliance target, lean toward buying.

2. Does the pricing scale with your footprint instead of your value? Per-filing, per-seat-you-can't-control, per-transaction on work that's the same script every time. If the vendor's cost is flat and yours is linear, that's a build trigger.

3. Is a mistake a regulatory penalty? If yes, stay bought until you can replay your build against historical results and prove it to the cent. No tests, no replay, no switch.

4. Does the vendor's license ban AI use, carry viral terms, or charge per filing? Any of those moves the tool up your build list. The Xero repricing is the live example: the moment a vendor governs what you do with your own data, the calculus changes.

Now the honest part. Building before you have the tests and the replay discipline is exactly how you get fined. The order matters. Ledger first because it's safe. Per-filing SaaS next because the math is obvious. Regulated rails last, and only behind proof. Skip the proof and you've traded a subscription for a liability.

I drew this line by replacing three of these tools across two real businesses, not by theorizing about it. I own the ledger. I own the tax filing. I built the payroll rails behind 172 tests and a penny-perfect replay. Each decision was unit economics and risk, not ideology.

If you're staring at a finance stack that costs more every quarter and locks your data behind terms you didn't write, that's the exact decision I help CEOs make. You can look at your own finance stack with me.

Ready to bring AI leadership into your company?

I work with a small number of companies at a time. If you're serious about AI, apply to work together and I'll review your application personally.

Get AI insights for business leaders

Practical AI strategy from someone who built the systems — not just studied them. No spam, no fluff.

Hodgen.AI

Ready to automate your growth?

Book a free 30-minute strategy call with Hodgen.AI.

Book a Strategy Call