A $52K Forensic Accounting Error: Where It Came From

How a $52,416 cash overstatement traced to a forensic accounting error: two keying mistakes a roll-forward formula carried forever. Here's the fix.

By Mike Hodgen

The Flag: A Regulator Spotted $55K That Didn't Add Up

An oversight party reviewing monthly financial filings for a business I keep the books for sent over a short note. They'd spotted something "weird, about $55k" on the reported cash-on-hand. Could we explain it.

When a regulator flags a number, you don't get to wave it off. You don't get to say "rounding" or "we'll fix it next quarter." You have to explain, line by line, exactly where the discrepancy came from and why it's there. That's the whole game with a forensic accounting error. The number isn't the problem. The inability to explain the number is the problem.

Here's the situation. A company under ongoing financial-reporting scrutiny. Books I'm responsible for. The reported cash on the monthly summary page had quietly drifted above what was actually sitting in the bank account. Nobody was accusing anyone of fraud. It was just a number that didn't reconcile to reality, and a reviewer with sharp eyes caught it.

The reviewer guessed "about $55k." When I traced it, the exact gap was $52,416.43.

That precision matters, because the only way to satisfy a regulator is to land on an exact figure with an exact origin. "Close enough" doesn't survive contact with someone whose job is to look closely.

And here's what makes these cases so dangerous. The discrepancy didn't appear all at once. It was built from small keying errors that compounded silently, month after month, inside a report that references its own prior output. Once a mistake gets into a self-referencing report, it doesn't go away. It rides forward forever until somebody external asks the question nobody internal thought to ask.

This is the story of where that $52,416.43 actually came from, and why your books might have the same bomb in them right now.

Why the Ledger Was Right and the Report Was Wrong

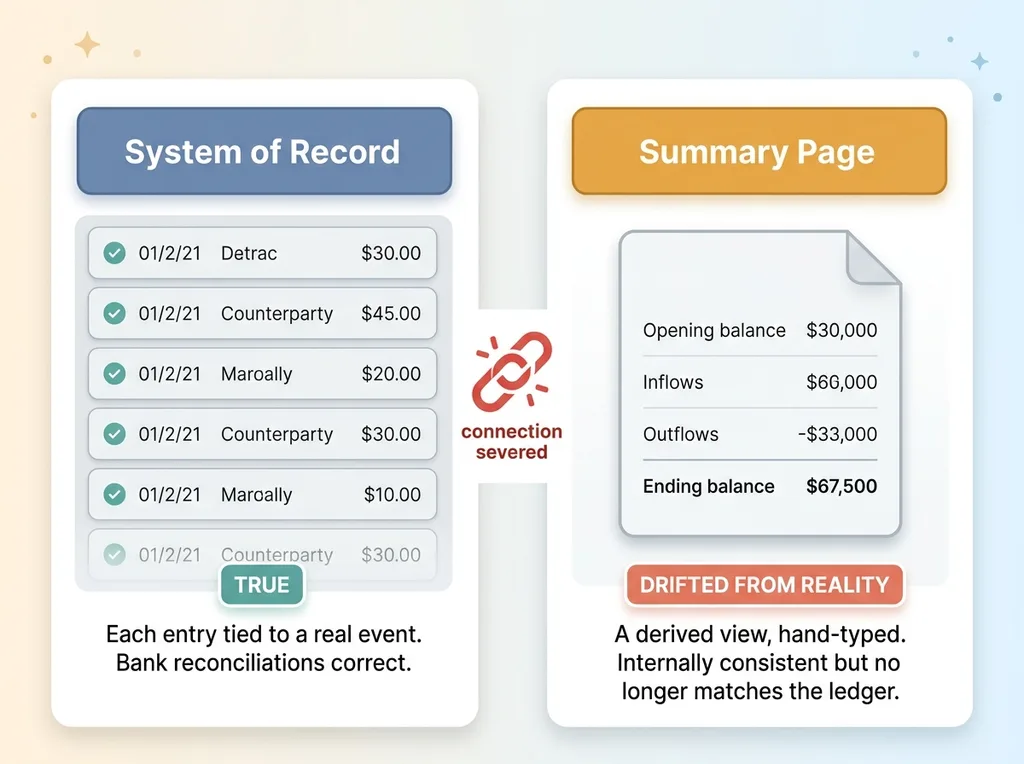

The system of record vs. the summary page

First thing I want to be clear about, because it's the part that builds trust with a regulator: the underlying ledger was correct. The bank reconciliations were correct. Every actual transaction was recorded properly in the system of record.

System of record vs. summary page

System of record vs. summary page

The defect lived in exactly one place. A summary page. The single sheet that gets filed monthly, summarizing where the cash stands.

This is a critical distinction. The system of record is where transactions live, each one tied to a real event with a real counterparty. The summary page is a derived view. It's supposed to reflect the system of record, but in this case it had drifted away from it. The truth was intact. The report on top of the truth was wrong.

How a roll-forward formula propagates errors

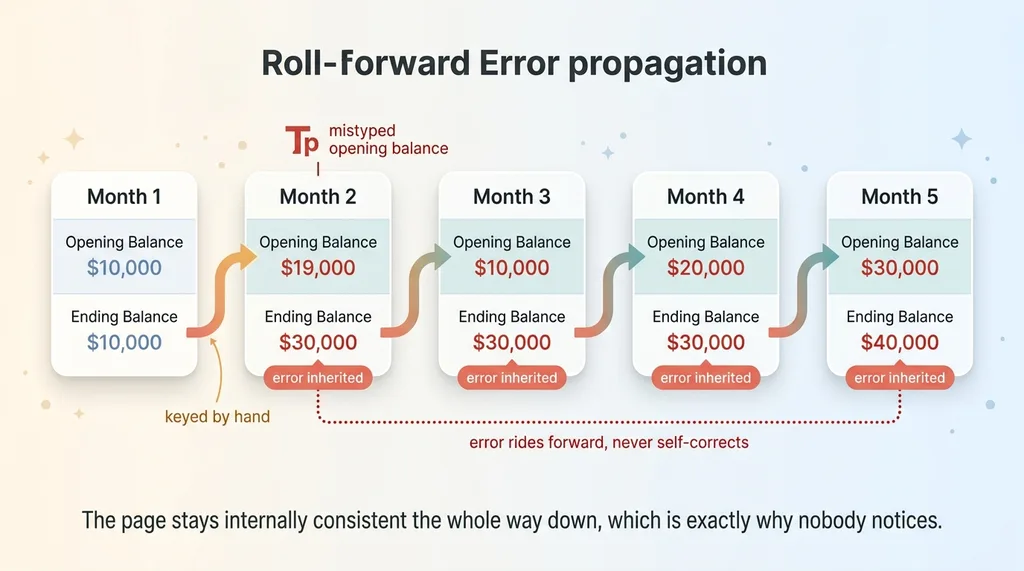

Here's the mechanic that caused it, and it's so ordinary that almost every business uses it.

Roll-forward error propagation

Roll-forward error propagation

Each monthly report takes its ending balance and carries it into the next month's opening balance. Month one ends at $100. Month two opens at $100. That's a roll-forward, and it's normal accounting. There's nothing wrong with the concept.

The danger is in how the opening figure gets there. On this summary page, the opening balance was keyed by a human. Typed in. Not re-derived from the actual ledger and bank data.

So picture what happens if one month's opening balance gets mistyped. Every subsequent month inherits the error. Month three opens with the wrong number because it copied month two. Month four copies month three. The report stays internally consistent the whole way down, which is exactly why nobody notices. It never self-corrects, because there's no point where the number gets re-anchored to reality. It just gets copied forward on faith.

This is a forensic accounting error in the structural sense, not a math sense. The arithmetic on the page was perfect. The page just stopped describing the real world. And like a lot of errors that stay silent until someone looks, it compounded quietly for years before anyone asked.

The Forensic Trace: Two Injection Events, Years Apart

To answer the regulator, I had to do the unglamorous work. I re-read every filed page, month by month, going back years. For each month I computed two numbers: the figure that was filed, and a clean figure re-derived from the actual ledger and bank data for that period.

Then I lined them up and looked for the months where the two diverged. If the report and reality agreed, that month was fine. If they split, that's an injection point. The exact period where a new error entered the running total.

I found exactly two.

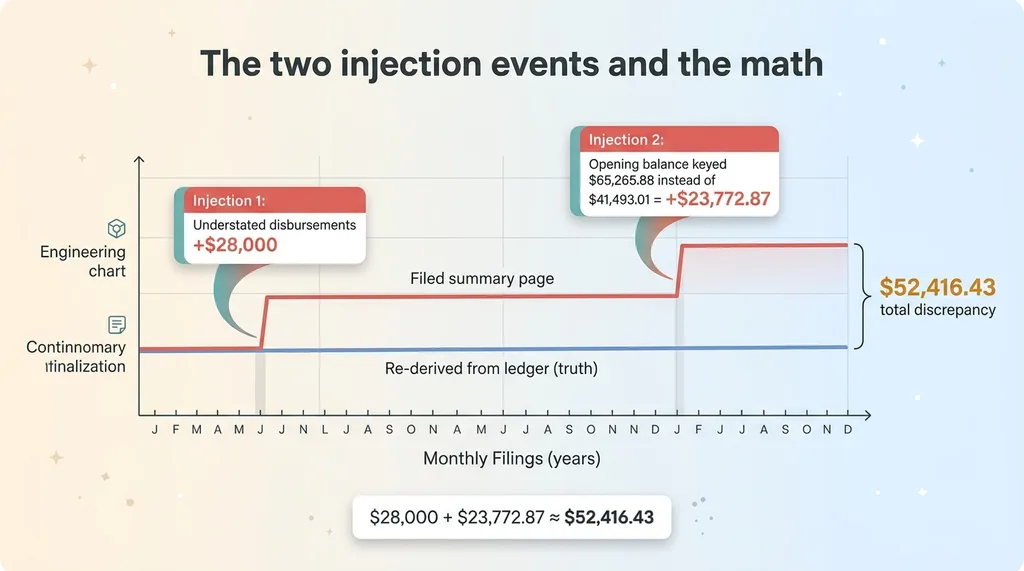

Injection one: ~$28K of understated disbursements

In one month, the summary page understated disbursements by roughly $28,000. Real money left the bank account that period. The transactions were in the ledger. But on the summary page, that outflow never got fully subtracted.

So the reported cash sat about $28k higher than it should have, starting that month. And because of the roll-forward, that inflated figure became the opening balance for the next month, and the next, and the next.

Injection two: an opening balance keyed as $65,265.88 instead of $41,493.01

The second injection happened in a completely different month, well apart from the first. A preparer keyed the opening balance as $65,265.88, when the prior month's true ending balance was $41,493.01.

The two injection events and the math

The two injection events and the math

That's a difference of $23,772.87. A typo. A tired human reading one line and typing another.

Now do the arithmetic on the two injections. About $28,000 from the understated disbursements, plus $23,772.87 from the mis-keyed opening balance. Add them and you land right around $52,416.43. The two ordinary mistakes, made years apart by people who weren't doing anything wrong on purpose, stacked into the exact gap the regulator flagged.

That's the whole lesson in one trace. No malice. No fraud. Just two of the most common errors a human makes when re-typing financial figures. But because the report carried numbers forward on faith, each one became permanent the moment it happened. The error didn't fade. It got locked in and then rode forward through every month after it.

How Small Data-Entry Errors Become Big Problems

This is the part business owners underestimate, so let me be direct about it.

A single mis-keyed figure on a self-referencing report does not stay small. It doesn't get diluted over time. It rides forward into every future period at full size, and the gap actually looks bigger and stranger the longer it sits, because it stacks with any other error that shows up later.

That's exactly what happened here. One injection was $28k. Another was $23.7k. Individually, either one might have been shrugged off as a fat-finger. Together, years apart, they produced a $52k discrepancy that looked alarming and inexplicable to an outside reviewer.

The reason these errors are so dangerous is that they're invisible from the inside. The summary page is internally consistent. Every row adds up. The opening plus the inflows minus the outflows equals the ending, perfectly. There's no broken formula to catch, no error cell flashing red. The page is internally coherent. It just doesn't match reality.

This is the structural fragility of any report that depends on a human re-typing the prior period's number. The whole structure rests on faith that last month's typed figure was correct, and that the month before that was correct, all the way back. One bad keystroke anywhere in that chain poisons everything downstream.

The fix isn't "be more careful." Careful people made both of these errors. The fix is structural: stop copying numbers forward and start re-deriving them. That's the difference between a number that's been recomputed from source and a number that's been copied forward on trust. It's the same reason I build a ledger that can't be wrong by design instead of a spreadsheet that hopes everyone types carefully.

The Fix: Deterministic Re-Derivation From Source

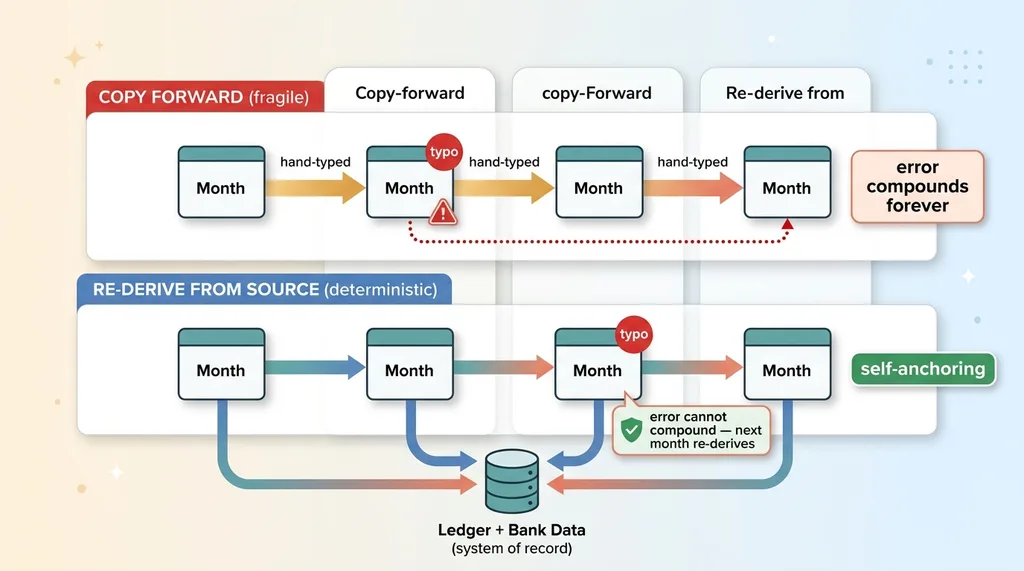

The solution to a roll-forward error is to stop trusting the roll-forward.

Recompute every month, never trust the carried-forward figure

Instead of keying each month's opening balance from the prior report, you re-derive every month's opening and ending balance directly from the ledger and bank data. The summary page becomes a computed view of the system of record, not a hand-typed running total that drifts on its own.

Copy-forward vs. re-derive from source fix

Copy-forward vs. re-derive from source fix

The moment I built that re-derivation, the two injection points lit up immediately. The re-derived line and the filed line agreed for most months, then diverged hard on one specific month, agreed again, then diverged on another. Those two divergence points were the injections. The investigation that took hours of manual page-by-page reading became something the computation surfaces instantly.

Code computes, the human reviews

I built this as a deterministic recomputation. No AI guessing at numbers. This is important and I want to be precise about it: a language model is great at reading filings, spotting where two lines diverge, and explaining what it found. It is terrible at arithmetic you can stake a regulatory filing on.

Division of labor: code computes, model reviews

Division of labor: code computes, model reviews

So the division of labor is strict. The model can help find the divergence and narrate the story. The math is done entirely by code that produces the same answer every single time. That's the principle I apply across every financial system I build: let the code do the math, and never let a model improvise a number that has to be exactly right.

The way you validate a figure like this is to replay every prior result from source. Recompute each month from the underlying data and check it against what was filed. If they match, you're clean. If they don't, you've found your injection point to the exact period and the exact dollar.

And here's the elegant part: the cure and the prevention are the same mechanism. A report that recomputes from source every period can't carry an error forever, because each month re-anchors to reality. A bad keystroke can still happen, but it can't compound, because next month doesn't inherit it. It re-derives instead.

What This Costs You When Nobody Catches It

This particular case ended fine. The regulator got a clean root-cause explanation, the exact figure, the two injection points, and a corrected number. Case closed.

But play out the version where nobody traces it.

A $52k discrepancy on a regulated filing that you cannot explain looks like fraud or incompetence, even when it's neither. The reviewer doesn't know your preparer fat-fingered an opening balance three years ago. They just see reported cash that doesn't match the bank, and a company that can't say why. That's a reputation problem with the exact party you least want one with.

Then there's the time cost. Tracing this meant re-reading every filed page going back years, re-deriving each month, and lining up the divergences. That's real hours, and they all happen under pressure, after the flag, on the regulator's timeline instead of yours.

But here's the lesson I actually want the business owner to take. If your monthly financials depend on someone re-keying last month's ending balance, you have this exact bomb sitting in your books right now. You won't know until someone external asks.

And most businesses never get audited closely enough to find it. That sounds like good news. It isn't. It means the gap just keeps growing, quietly, with no external pressure to ever surface it. The companies that get caught are the lucky ones. They at least get to fix it.

If Your Books Carry Numbers Forward by Hand, You Have This Risk

Most small and mid-size businesses run on summary pages and spreadsheets that copy figures forward. And in my experience, most of them have at least one quiet drift like this hiding somewhere in the carried-forward numbers.

The fix isn't more careful typing. People who type carefully made both errors in this case. The fix is building reporting that re-derives from source, so a single keying error can't compound into a $52k surprise on a regulated filing.

That's the work I do. I find the injection points, I trace the exact dollar and the exact period, and I rebuild the reporting so the numbers re-anchor to reality every period instead of riding forward on faith.

If you've ever had a balance that "just looks a little off" and nobody on your team can say why, that's the symptom. It's usually not nothing. It's usually a carried-forward number that stopped matching the bank a while ago and quietly got worse.

That's the kind of forensic-and-rebuild work I take on. Find the error, explain it precisely, then make the structure so the error can't happen again.

Thinking about AI for your business?

If this resonated, let's have a conversation. I do free 30-minute discovery calls where we look at your operations and identify where AI could actually move the needle.

Get AI insights for business leaders

Practical AI strategy from someone who built the systems — not just studied them. No spam, no fluff.

Hodgen.AI

Ready to automate your growth?

Book a free 30-minute strategy call with Hodgen.AI.

Book a Strategy Call