How AI Catches Chargebacks Before They Happen

I built an AI chargeback prevention system for my ecommerce brand that replaced Chargeflow. Here's how it works, what it costs, and why it pays for itself.

By Mike Hodgen

Last year, chargebacks cost my DTC fashion brand just over $15,000. That's not the disputed transaction value — that's the fees, lost product, and recovery costs on top of the revenue I'd already lost. When I started tracking it closely, AI chargeback prevention ecommerce wasn't even a category I was thinking about. I was just trying to stop the bleeding.

The pattern was maddening. A customer buys a handmade piece, it ships from our San Diego studio, tracking shows delivered, and three weeks later I get a chargeback notification claiming "unauthorized transaction." Or the classic: "item not received" on a package with signature confirmation. Friendly fraud — the kind where the customer absolutely received the product but found it easier to call their bank than to email us.

I tried Chargeflow first. It's a solid tool for what it does, which is automating dispute responses. But the business model never sat right with me. They charge roughly 25% of recovered chargebacks as a success fee. That means I'm paying a premium for someone to fight fires that already burned down the kitchen. The incentive structure is backwards — they make more money when I have more chargebacks. They have no financial reason to help me prevent them.

So I decided to build something different. Not a dispute response tool. A prevention system.

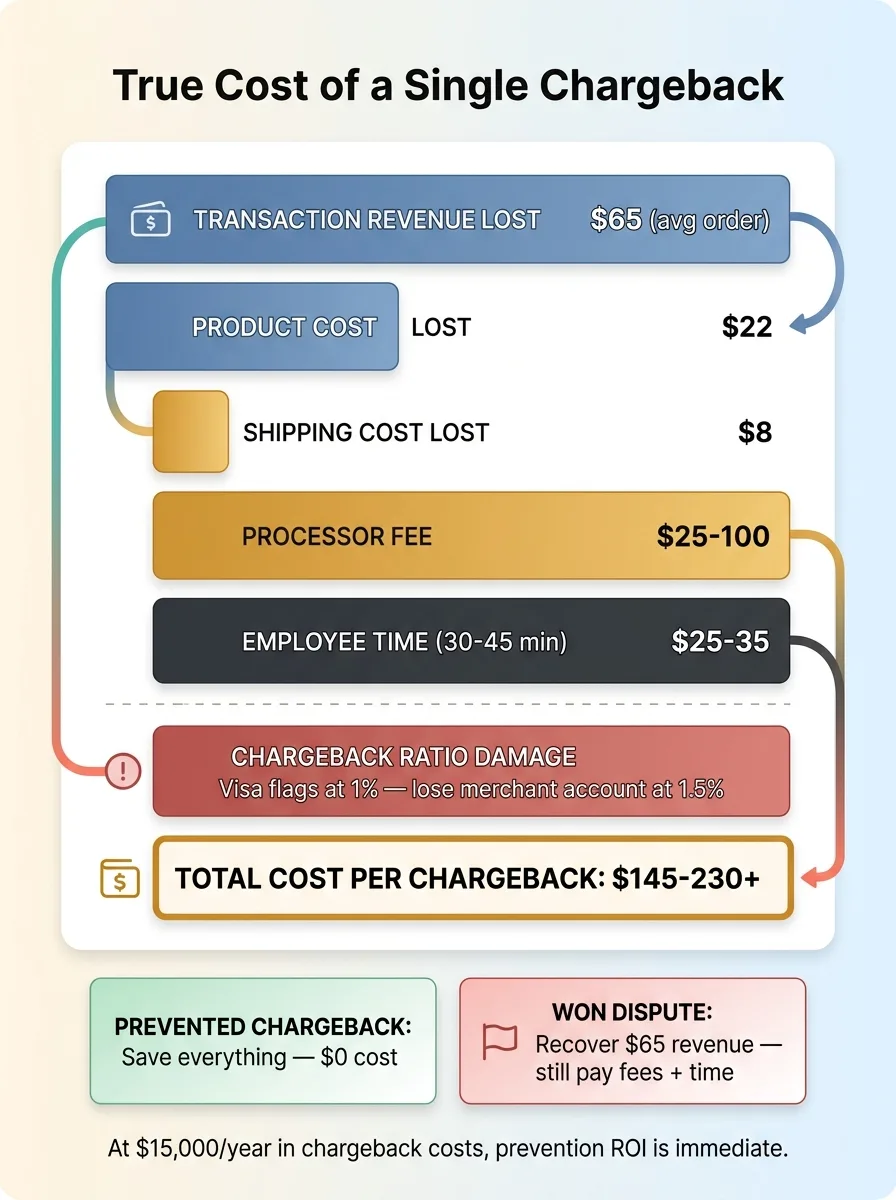

Here's the math that motivated me. Every chargeback carries a $25-$100 fee from the payment processor regardless of outcome. You lose the product, you lose the shipping cost, you lose the transaction revenue, and you burn 30-45 minutes of employee time compiling evidence for a dispute you'll probably lose anyway. The industry average merchant win rate on disputes is somewhere between 20-30%. Those are terrible odds.

And then there's the existential threat: your chargeback ratio. Visa and Mastercard flag merchants who exceed a 1% chargeback-to-transaction ratio. Go above 1.5% and you risk losing your merchant account entirely. For a DTC brand, that's not a setback — that's a shutdown.

How Chargebacks Actually Work (And Where AI Intervenes)

The Chargeback Timeline Most Merchants Don't Understand

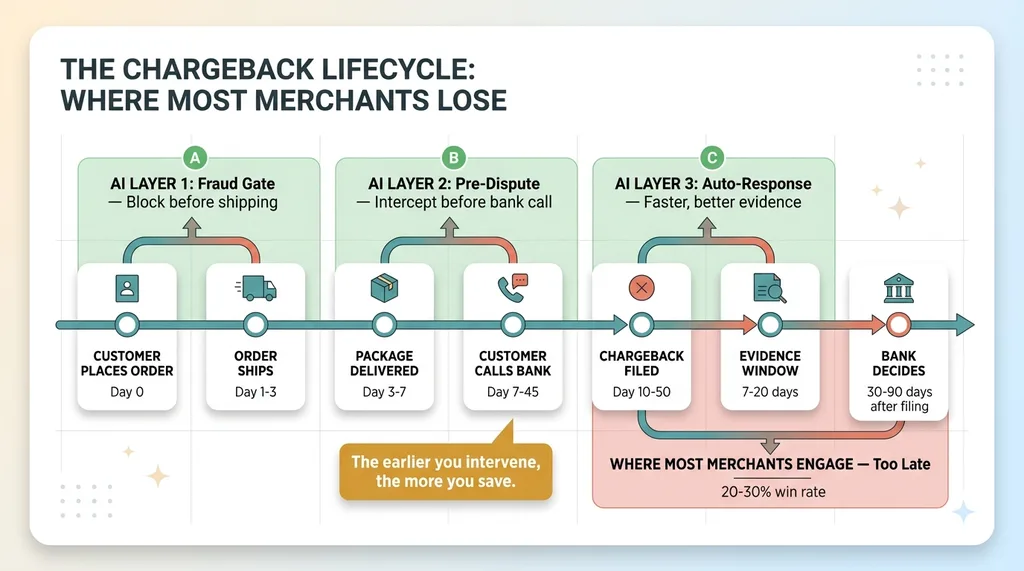

Most merchants think of a chargeback as a single event. It's not. It's a lifecycle with distinct stages, and each stage has a window where you can act — or miss your chance.

Chargeback Lifecycle Timeline with AI Intervention Windows

Chargeback Lifecycle Timeline with AI Intervention Windows

Here's how it works. A customer makes a transaction. Days or weeks later, they call their bank and dispute the charge. The issuing bank files a chargeback with the card network. The payment processor notifies you, the merchant. You now have a narrow evidence window — typically 7-20 days depending on the card network — to respond with documentation proving the transaction was legitimate. Then the bank decides.

The problem is that most merchants only engage at that evidence stage. By then, you've already lost the product, the customer relationship is adversarial, and you're playing defense with a referee who's biased toward the cardholder.

Three Intervention Points That Actually Matter

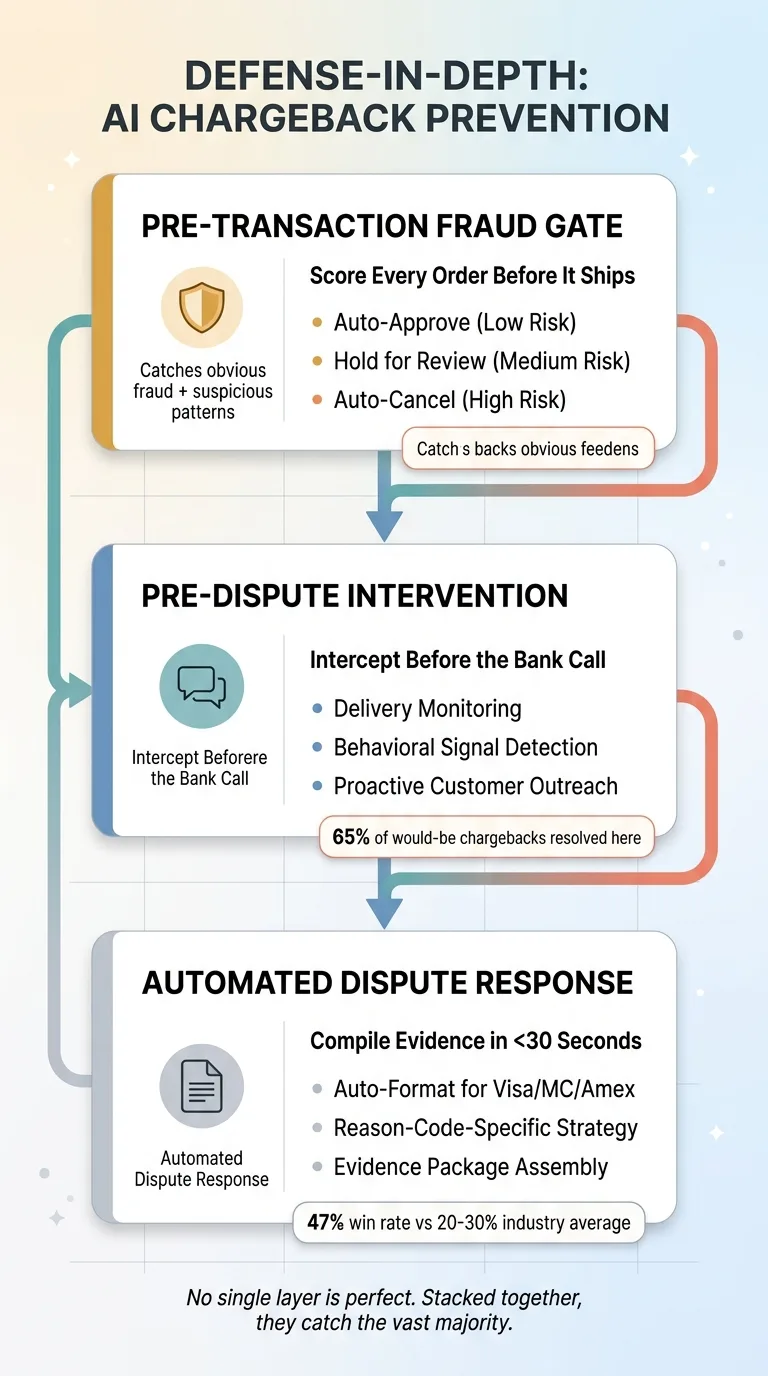

The system I built operates on a defense-in-depth philosophy. Three layers, each catching what the previous one missed.

Three-Layer Defense-in-Depth Chargeback Prevention System

Three-Layer Defense-in-Depth Chargeback Prevention System

Layer 1: Pre-transaction fraud gate. Score every order before it ships. Block the ones that are obviously fraudulent, hold the suspicious ones for review.

Layer 2: Pre-dispute intervention. After the order ships, monitor for signals that a customer is heading toward a chargeback — and intercept them before they call their bank.

Layer 3: Automated dispute response. When a chargeback does come through, compile evidence and respond instantly in the format the card network expects.

No single layer is perfect. But stacked together, they catch the vast majority of chargebacks before they become chargebacks.

The Fraud Gate: Blocking Bad Orders at the Door

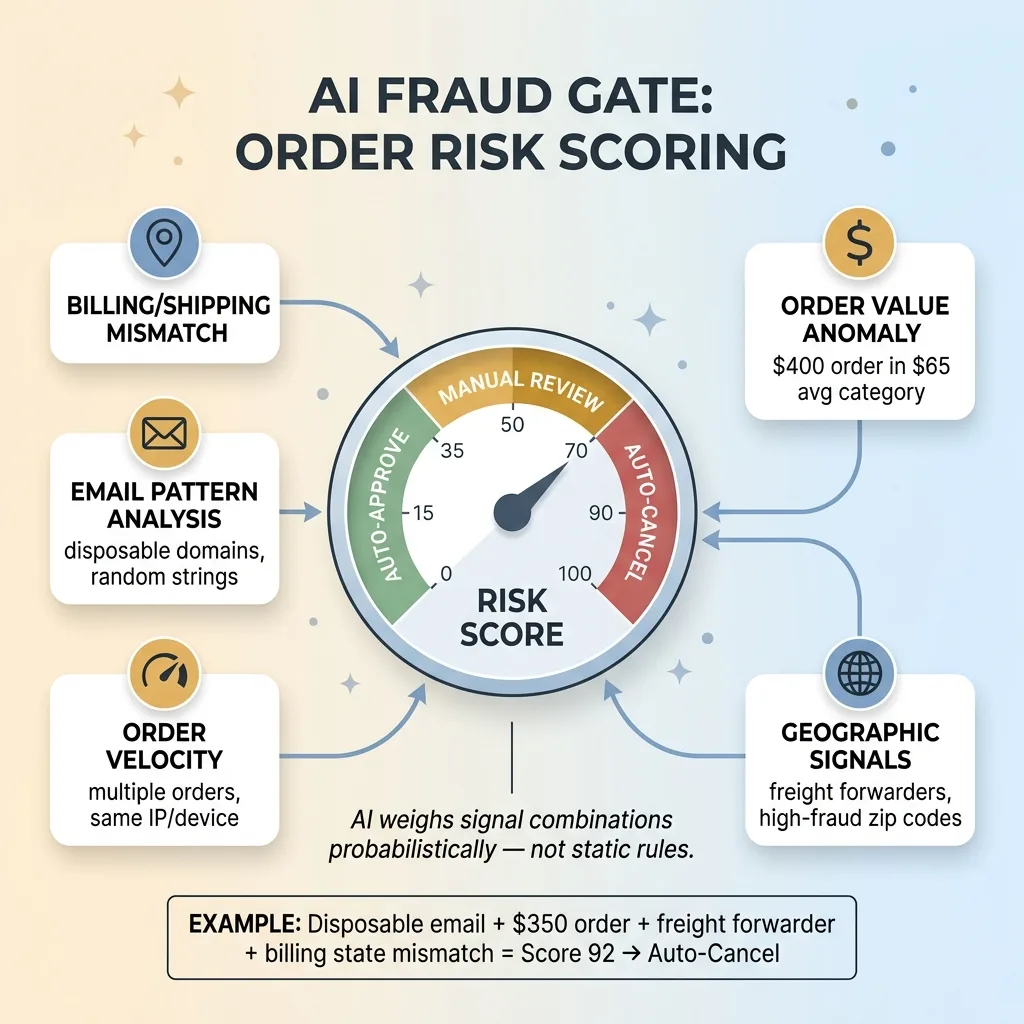

What the AI Scores on Every Order

A webhook fires on every new order that hits our Shopify store. The AI evaluates multiple signals and produces a risk score from 0 to 100.

Fraud Scoring Signal Analysis

Fraud Scoring Signal Analysis

Here's what it's looking at:

- Billing/shipping address mismatch — not always fraud, but a strong signal when combined with other factors

- Email pattern analysis — disposable email domains, recently created addresses, randomized character strings

- Order velocity — multiple orders from the same IP or device fingerprint in a short window

- Order value anomalies — a $400 order on a product category that averages $65 gets flagged

- Geographic signals — shipping to known freight forwarder addresses, zip codes with high fraud concentration, international orders to regions with elevated chargeback rates

Below a certain threshold, the order auto-approves and ships normally. Above a second threshold, it's held for manual review. Way above — like a disposable email placing a $350 order to a freight forwarder with a billing address in a different state — it auto-cancels with a polite message directing the customer to contact us if the order is legitimate.

The False Positive Problem

This is where most fraud detection systems fail, and honestly where my early version failed too.

About two months after launch, I got an angry email from a legitimate customer. She'd placed an order for eight pieces — gifts for her bridesmaids. The system saw the high order value, a shipping address different from billing (she was shipping to the wedding venue), and flagged it as fraud. Auto-cancelled. She was not happy.

That one hurt. It was a $520 order from a real customer, and I'd turned her away because the system was too aggressive.

The fix wasn't lowering the threshold across the board — that would have let actual fraud slip through. Instead, I built a feedback loop. Every confirmed fraud case and every confirmed legitimate order that got flagged feeds back into the scoring model. Over six months of tuning with real outcome data, false positives dropped by roughly 60% while fraud catch rate actually improved.

The system gets smarter because it learns from its own mistakes. That's the difference between a static rules engine and an AI-powered approach. A rules engine says "flag all orders over $300 with address mismatch." The AI says "this specific combination of signals, at this magnitude, given what I've seen before, produces this probability of fraud."

Pre-Dispute Intervention: Catching Problems Before the Bank Hears About Them

This is the highest-ROI layer. It's also the one most merchants completely ignore.

Delivery Confirmation Triggers

The system monitors delivery status via tracking webhooks from our shipping provider. It's watching for a specific pattern: package shows "delivered" but the customer hasn't opened the delivery confirmation email, hasn't visited the site, and hasn't engaged with any post-purchase touchpoint.

That silence is a signal. It doesn't always mean trouble. But when you combine it with other factors — a first-time customer, a high-value order, a delivery to an apartment complex where porch theft is common — it's worth a proactive touch.

The system also watches for behavioral red flags after purchase: a customer who changes their email address shortly after ordering, or one who contacts support multiple times asking "when will this arrive" with escalating urgency. That anxiety pattern precedes "item not received" chargebacks about 40% of the time in our data.

The Proactive Outreach Sequence

When these signals fire, the system triggers a proactive check-in. Not a generic "how was your order?" email — a specific, human-feeling message that acknowledges the delivery and asks if everything arrived safely. If the customer responds with a problem, it routes directly to our AI customer support system that handles returns and exchanges, which is built to resolve issues quickly and with minimal friction.

Here's the key insight that changed how I think about chargebacks: most "friendly fraud" isn't actually fraud. It's frustrated customers who couldn't get a fast enough resolution through normal channels. They didn't set out to steal from you. They wanted a refund or a replacement, hit a wall (slow email response, confusing return policy, no phone number), and called their bank because that felt like the only option.

When you intercept those customers with fast, empathetic support before they pick up the phone, you convert a chargeback into a return or exchange. Yes, you might still lose the sale. But you save the $25-100 fee, you protect your chargeback ratio, and you often save the customer relationship entirely.

In our data, roughly 65% of would-be chargebacks get resolved at this pre-dispute stage. That's the number that made the entire system worth building.

Automated Dispute Response: When Prevention Fails

Evidence Compilation in Seconds

Some chargebacks are going to happen no matter what. The customer is genuinely dishonest, or they truly didn't receive the package, or the product had a defect you didn't catch. When a chargeback notification hits, the system needs to respond fast and respond well.

A webhook from our payment processor triggers automated evidence compilation. The system pulls and assembles: order details with timestamps, shipping confirmation and carrier tracking data, delivery proof including GPS coordinates if available, all customer communication history (email, chat), the IP address and device information from checkout, the fraud risk score assigned at time of purchase, and product photos matching the SKU ordered.

All of this gets formatted into the specific evidence structure that Visa, Mastercard, and Amex expect. Different card networks want different things. The system knows which.

Response Templates That Actually Win

Different chargeback reason codes demand different strategies. An "unauthorized transaction" dispute needs AVS match data, device fingerprinting, and proof the customer's IP was consistent with their billing address. An "item not received" dispute needs delivery confirmation, GPS data, and the proactive outreach emails showing the customer was contacted. An "item not as described" dispute needs product photos, the listing copy, and any customer communication where the product was discussed.

The AI categorizes the reason code and assembles the appropriate evidence package. A manual dispute response used to take one of my team members 30-45 minutes. The automated version completes in under 30 seconds.

Our win rate on automated responses runs around 47%. That's roughly double the industry average of 20-30%. It's not magic — it's just faster, more thorough evidence that's formatted exactly how the card networks want to see it.

The Economics: What This Actually Costs vs. What It Saves

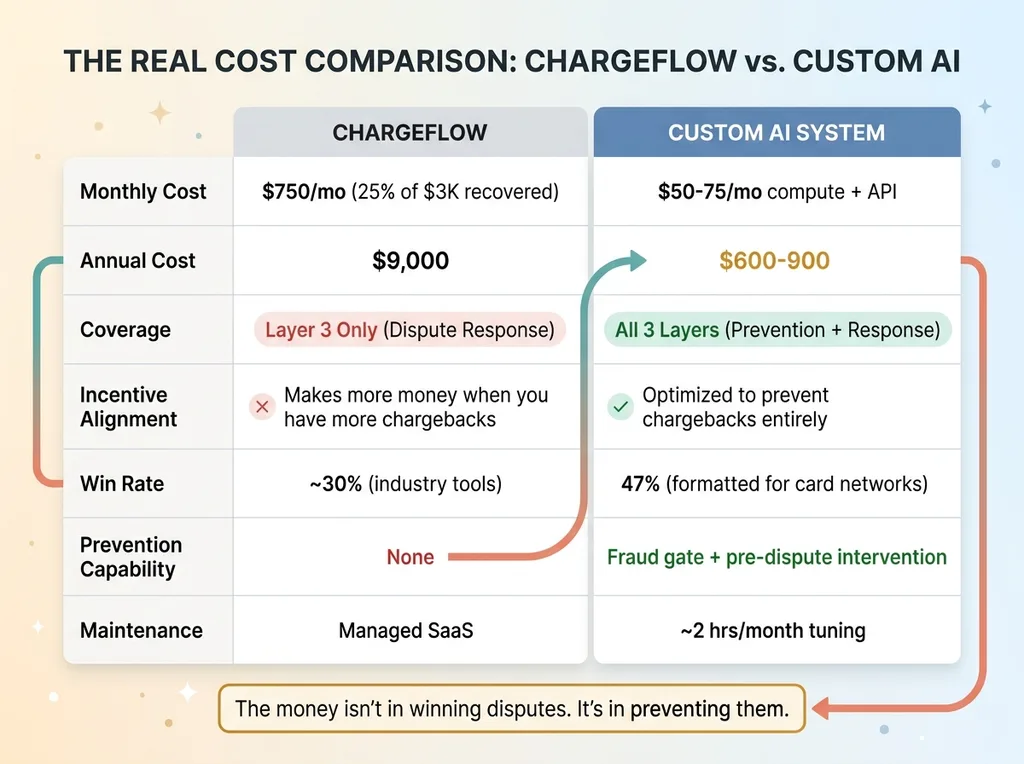

Chargeflow vs. Custom: A Real Cost Comparison

Let's do the math. Chargeflow charges approximately 25% of recovered chargebacks. If you're recovering $3,000/month in disputed transactions, that's $750/month going to Chargeflow. Over a year: $9,000. And that only covers Layer 3 — dispute response. No prevention.

Chargeflow vs Custom AI System Cost Comparison

Chargeflow vs Custom AI System Cost Comparison

My custom system's marginal cost is minimal because it's built into the broader ecommerce automation platform. The webhook infrastructure, AI scoring, and response automation run on compute that costs pennies per transaction. Call it $50-75/month in total compute and API costs. Maintenance time averages maybe two hours a month for threshold tuning and model review.

But here's the real economic argument: the money isn't in winning disputes. It's in preventing them.

A prevented chargeback saves the full order value, plus the $25-100 processor fee, plus your chargeback ratio stays clean. A won dispute only recovers the transaction value — you've already paid the fee and burned the time. This same ROI logic applies to the dynamic pricing system I built to manage 500+ products. Automation doesn't just save money on the task. It changes the economics of the category entirely.

The Hidden Cost Nobody Talks About

Before this system existed, someone on my team spent 6-8 hours per week on chargeback-related work. Reviewing flagged orders, compiling evidence, submitting disputes, tracking outcomes, stressing about the chargeback ratio.

True Cost of a Single Chargeback

True Cost of a Single Chargeback

That's over 350 hours a year. At even a modest hourly cost, that's significant. But the real cost isn't the dollars — it's the opportunity cost. That person now spends those hours on product development and customer experience work that actually grows revenue. Getting operational drag off your best people is one of the most undervalued returns on AI investment.

Building Chargeback Prevention Into Your Ecommerce Stack

If you want to build something like this, here's what it requires: webhook infrastructure (Shopify, WooCommerce, BigCommerce all support this), an AI layer for scoring and decision-making, integration with your customer support and fulfillment systems, and someone who understands both the technical architecture and the business logic of ecommerce fraud prevention.

I'll be honest — not every brand needs a fully custom system. If you're doing under $500K in revenue and your chargeback volume is manageable, a tool like Chargeflow is probably the right call. Use it, and focus your energy elsewhere.

But once you're past that point, the economics of custom shift fast. This is especially true if you're already building AI systems across other parts of the business. The Chargeback Guard is one of 14 skills in the AI platform I built to run my brand. Each skill feeds data to the others. The customer support system tells the fraud gate which customers had issues. The fraud gate's scoring data improves the dispute response templates. The delivery monitoring informs the customer support routing. It's a connected system, not a collection of disconnected tools.

That interconnection is where the real value compounds. And it's why having someone build these systems as a coherent whole — rather than bolting on point solutions one at a time — matters more than most operators realize.

Want to Explore What AI Chargeback Prevention Could Look Like for Your Brand?

If chargebacks are costing you real money — or worse, putting your merchant account at risk — and you want to understand what a custom prevention system would look like for your specific business, let's talk.

No pitch deck. No sales team. Just a direct conversation about your operations, your pain points, and where AI makes practical sense.

Book a Discovery Call — 30 minutes, zero obligation.

Get AI insights for business leaders

Practical AI strategy from someone who built the systems — not just studied them. No spam, no fluff.

Hodgen.AI

Ready to automate your growth?

Book a free 30-minute strategy call with Hodgen.AI.

Book a Strategy Call