AI Real Estate Underwriting for a Niche No Tool Covers

Generic CRE tools can't model adaptive-reuse deals. Here's the AI real estate underwriting niche tool I built, and why depth beats breadth.

By Mike Hodgen

The Tool That Almost Worked, Except for the Parts That Mattered

A developer reached out who works in one of the strangest corners of commercial real estate: adaptive reuse. Taking old buildings (a worn-out warehouse, a defunct school, a former bank) and converting them into something new. Apartments, hotels, mixed-use. It's a real business with real money behind it, and it lives in a part of the market that no off-the-shelf software actually models.

He'd been trying to underwrite his deals with the standard tools. The big CRE underwriting platforms. The syndication-management software. And on paper they should have worked.

They handled a generic apartment acquisition fine. They handled an office building fine. But they ignored the three things that actually decide whether one of his deals pencils. The layered tax credits. The conversion from as-built construction costs to a stabilized proforma. And construction-cost integration carried through the whole model.

So here's what he was actually doing. Rebuilding the same spreadsheet by hand for every deal. Then re-keying the outputs into an investor portal that didn't speak the same language as his underwriting. Two sources of truth, neither of them complete, both of them manual.

This is the gap that AI real estate underwriting in a niche is supposed to close, but most people get the diagnosis wrong. They assume the problem is that the AI isn't smart enough yet. It isn't. The problem is that nobody bothered to model his vertical in the first place.

The incumbents weren't failing at adaptive reuse. They were ignoring it on purpose. It's a small slice of their addressable market, and building for it doesn't move their numbers.

That neglect is the whole opportunity. When I looked at his workflow, I wasn't seeing a technology problem. I was seeing a modeling problem that happened to be solvable with the right plumbing underneath it.

Why Generic CRE Underwriting Skips Adaptive-Reuse Deals

Generic CRE tools vs. Vertical adaptive-reuse tool comparison

Generic CRE tools vs. Vertical adaptive-reuse tool comparison

Tax credits the big tools treat as a footnote

Adaptive-reuse economics don't hinge on a single tax credit line item. They hinge on stacking several at once. Historic rehabilitation credits. Energy credits. Local and state incentives that change by jurisdiction. These layer and interact with each other, and the order and structure of the stack changes what the deal returns.

Generic CRE tools give you one field for "tax credit." Sometimes not even that. They were built for buyers of stabilized assets, where credits are a footnote, not the engine.

For this developer, the credit stack wasn't a footnote. It was frequently the difference between a deal that worked and a deal he passed on. A model that treats it as one number is modeling a different business than the one he runs.

As-built-to-proforma is its own discipline

The second blind spot is the construction side. He's not buying a finished building that throws off rent on day one. He's converting one. That means the model has to carry construction costs all the way through to a projected stabilized proforma.

That's not a single cost input. It's timing. Draw schedules. Contingency reserves. The gap between when money goes out and when the building actually stabilizes and produces income. Adaptive reuse deal modeling is its own discipline, and generic tools simply don't have the fields for it.

Why do the incumbents skip all this? Because their incentive is breadth. They serve the widest possible market, and the widest market buys stabilized apartments and offices. Building deep support for a niche this specific costs them engineering time they'd rather spend on features that touch a thousand customers.

Their breadth is their moat. It's also their blind spot. And that blind spot is exactly where a vertical tool wins. The moat for a niche player isn't the technology. It's the niche.

What I Actually Built: A Vertical Deal Analyzer

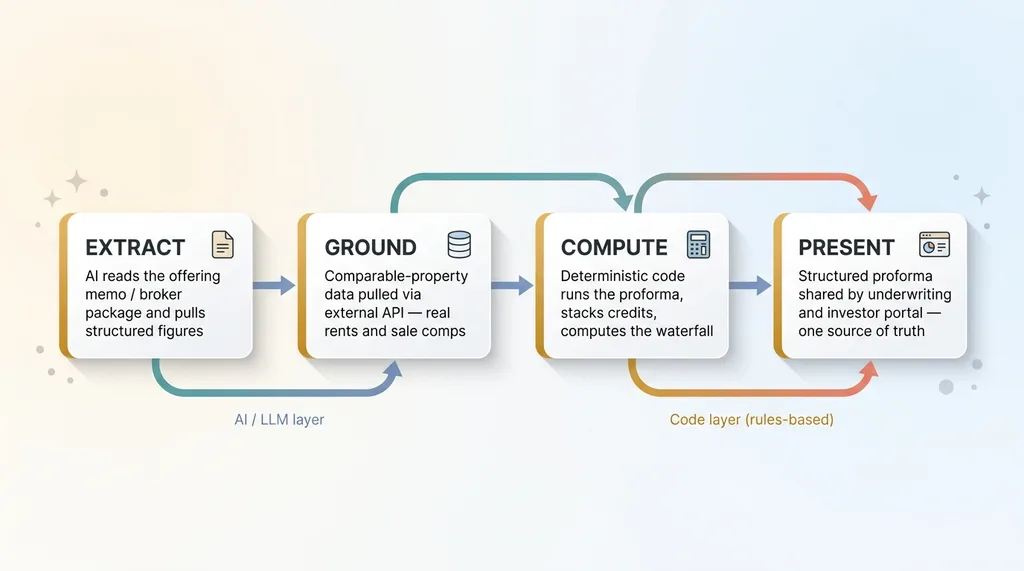

The extract-ground-compute-present pipeline architecture

The extract-ground-compute-present pipeline architecture

Ingest the deal document, not a blank form

The first decision was the most important one. Instead of making him fill out sixty form fields, the system ingests the deal document directly. The offering memo. The broker package. Whatever the seller's side actually sends.

AI extraction reads that document, pulls the relevant figures, and structures them. The starting point isn't a blank screen. It's the deal as it actually arrived in his inbox. That alone killed most of the manual re-keying that had been eating his time.

Comparable-property data via API

A model is only as good as its assumptions, and assumptions float away from reality fast if nobody anchors them. So the system pulls comparable-property data through an external data API.

That grounds the underwriting in the actual market. Rents, sale comps, the numbers a deal in this corner of real estate should clear. The AI doesn't get to guess what a comp looks like. It gets the real ones and works from there.

I'll be honest about how I got up to speed on a vertical this specialized this fast. I lean hard on range over depth across industries. I've built systems for financial advisory, manufacturing, labor compliance, healthcare. The domain changes, the pattern of "extract, ground, compute, present" doesn't. That lets me ramp on an unfamiliar vertical in days instead of months.

A structured proforma with the niche's real levers

The output is a structured proforma where the niche's real levers are first-class inputs, not afterthoughts. The layered credit stack is modeled as a stack. The construction-to-stabilized conversion is carried through with its timing and draws. This is the syndication deal analyzer the off-the-shelf tools never bothered to build.

And the investor side lives in the same system. The underwriting and the capital raise share one source of truth. No more re-keying a finished model into a portal that doesn't understand it. The proforma the developer runs is the proforma his investors see.

Where AI Does the Judging and Code Does the Math

This is the part I care most about getting right, because it's where most AI underwriting tools quietly fall apart.

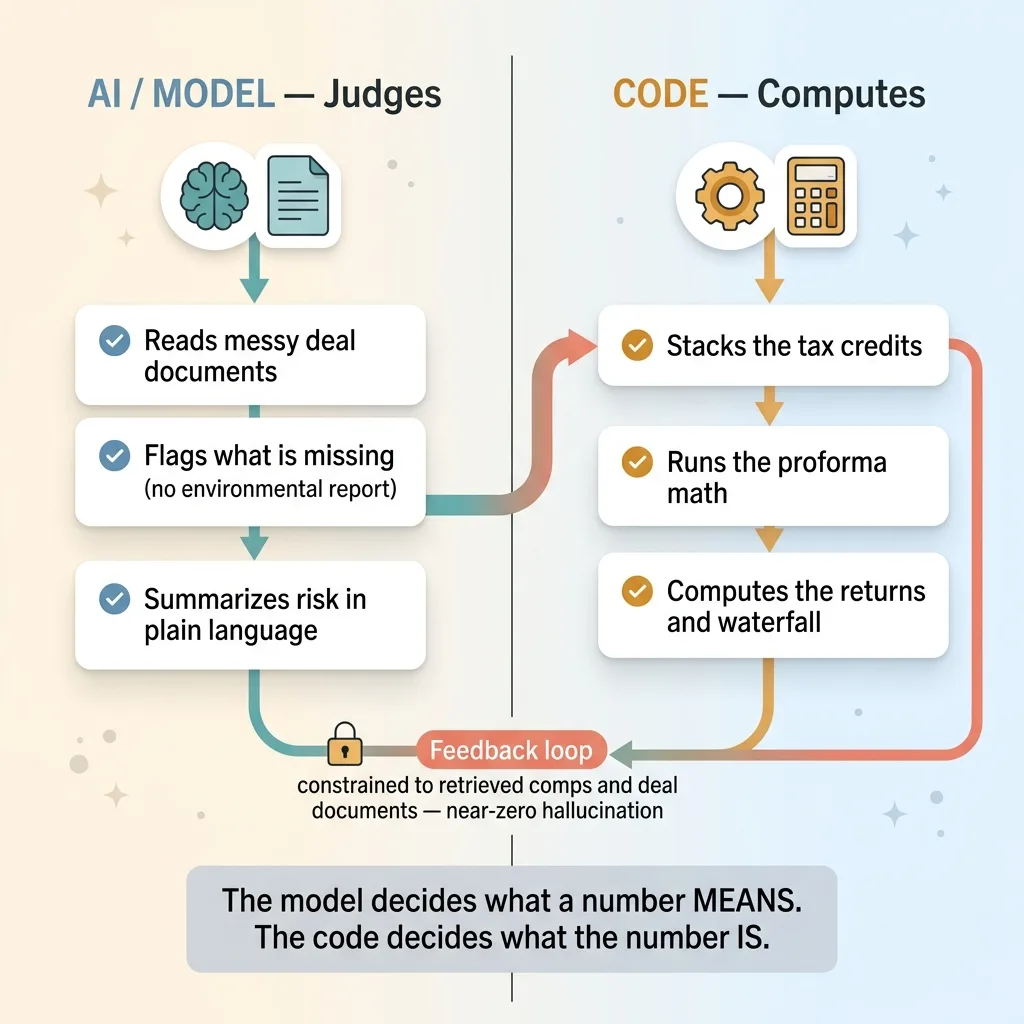

AI judges, code computes, the clean architectural split

AI judges, code computes, the clean architectural split

AI is genuinely good at some things here. Reading a messy, inconsistent deal document and pulling out the right figures. Flagging what's missing (no environmental report, no clear credit eligibility). Summarizing risk in plain language a busy operator can scan in thirty seconds. That's real work, and the LLM does it well.

AI is bad at being trusted with a financial waterfall. It should never be the thing computing returns, stacking credits, or running the proforma math. Language models are pattern matchers, not calculators, and a hallucinated number inside an investment decision is how you lose someone's money.

So the architecture splits the job cleanly. The model extracts and proposes. Deterministic code computes. The proforma, the credit stacking, the returns, the waterfall: all of that runs through actual code with actual rules. Nothing money-moving depends on an LLM doing arithmetic.

This is the principle I write about in let the model judge, let the code compute. The model decides what a number means. The code decides what the number is. Keep those two jobs separate and you get the speed of AI without betting the deal on its math.

The grounding matters just as much. The AI's outputs are constrained to the comparable data and the deal's own documents. It can't invent a comp because it's locked to the ones the API returned. This is the same discipline I describe in lock the AI to a fixed source of truth. When the model can only reference real, retrieved values, the hallucination risk drops to near zero.

That's the answer for the skeptic in the room. Yes, AI hallucinates. No, it isn't anywhere near the numbers that matter.

The Moat Is the Niche, Not the AI

Here's the part that surprises people. The AI was the easy part.

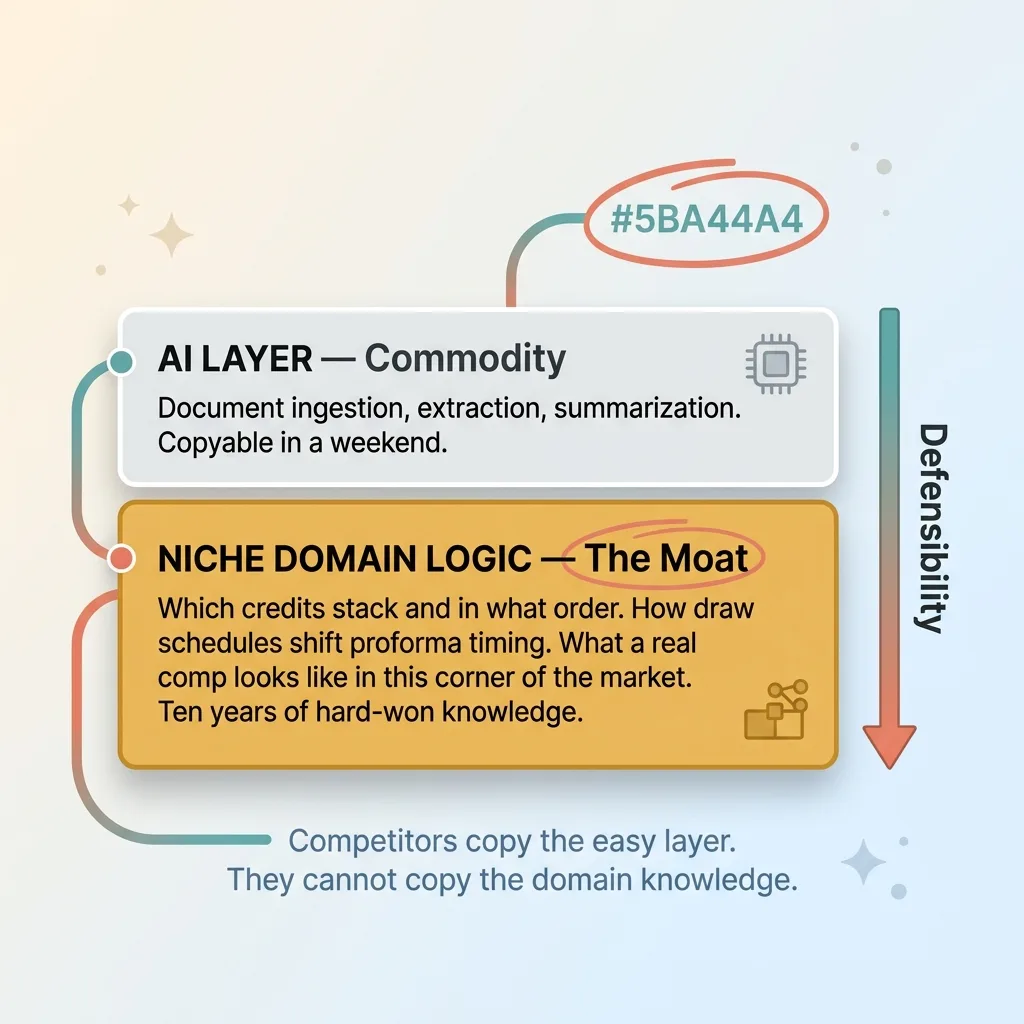

The moat is the niche, not the AI

The moat is the niche, not the AI

Any competent team can wire up document ingestion and an LLM. The extraction, the summarization, the structured output, that's all commodity now. If that were the hard part, the big platforms would have shipped it already.

What's genuinely hard to copy is encoding the domain. Knowing which credits actually stack and in what order. Understanding how the construction draw schedule shifts the proforma's timing. Knowing what a real comp looks like in this specific corner of the market, not the generic version.

None of that knowledge came from a model. It came from the developer. Years of doing these deals, getting some wrong, learning the rules nobody wrote down. The system just captured what was already in his head and made it run on every deal automatically.

That's the whole argument. The AI is a commodity layer. The niche logic is the defensible part. A competitor can copy your document ingestion in a weekend. They can't copy ten years of knowing how adaptive-reuse deals actually work.

This is why the wedge is almost never the impressive technology. It's the unglamorous domain modeling underneath. I've written before that the wedge is usually boring plumbing, and this is a textbook case. The interesting part of the system, from a buyer's perspective, is the credit-stacking logic. The interesting part from a technologist's perspective is nothing. It's just code that encodes rules.

The broader point for anyone in a specialized industry: the generic tool's blind spot is your advantage. A tool that's deep in your vertical beats one that's broad everywhere, every time, on the deals that actually matter to you. Breadth loses to depth where the money is.

What This Means If You're in an Industry the Big Tools Ignore

You don't need a category-defining platform

Let me answer the doubt directly, because I hear it constantly. "Generic AI tools can't model my specifics." Right. That's not the problem. That's the point.

The value isn't in building something broad enough to serve everyone. It's in building something deep enough to serve you, in a vertical the big players have decided isn't worth their engineering time. Their decision to skip you is your opening.

You don't need a venture-scale SaaS platform. You need a tool that knows your corner of the world cold, runs the math you currently run by hand, and saves you the hours you lose rebuilding the same model every week.

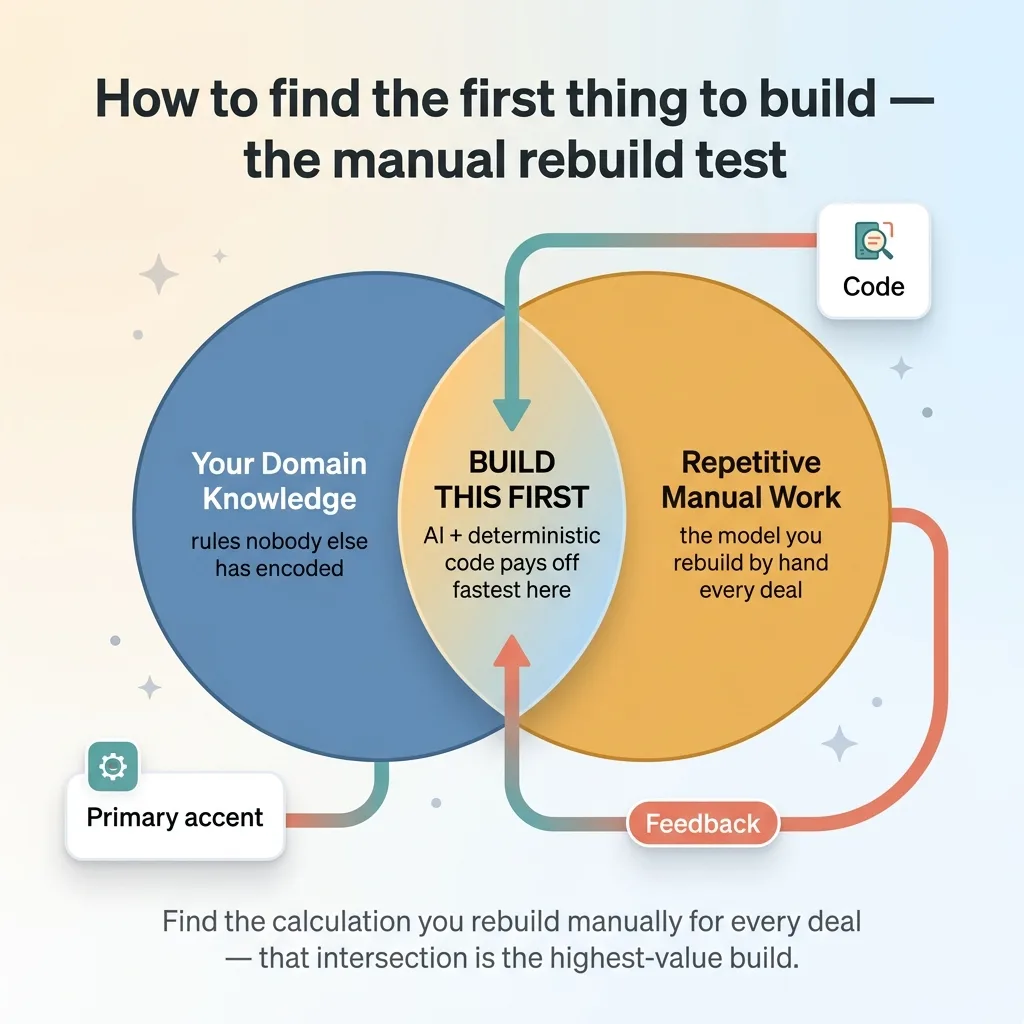

Start with the one model you rebuild by hand every week

Here's the practical lens I'd use. Find the calculation or workflow you rebuild manually for every deal, every job, every client. The one with rules nobody else has bothered to encode because they're specific to how your business actually works.

How to find the first thing to build, the manual rebuild test

How to find the first thing to build, the manual rebuild test

That's the highest-value thing to build first. Not because it's flashy, but because it's the exact spot where your domain knowledge meets repetitive manual work. That intersection is where AI plus deterministic code pays off fastest.

And let me be honest about what this isn't. It's not a land grab for a new software category. It's not a billion-dollar TAM play. It's an operational edge for an operator who knows the niche cold and is tired of doing the same modeling by hand. The developer didn't want to be a software company. He wanted his deals underwritten faster and cleaner. That's a smaller goal, and a much more achievable one.

If you've got a model or a process living half in spreadsheets and half in someone's head, that's exactly the kind of thing I build. The niche logic comes from you. The plumbing that makes it run on every deal comes from me.

Want to explore what AI could do for your business?

Book a free 30-minute strategy call. No pitch deck, no sales team, just a real conversation about your operations and where AI actually fits.

Get AI insights for business leaders

Practical AI strategy from someone who built the systems — not just studied them. No spam, no fluff.

Hodgen.AI

Ready to automate your growth?

Book a free 30-minute strategy call with Hodgen.AI.

Book a Strategy Call