Embedded Lending in Vertical SaaS: The Data Edge

Embedded lending in vertical SaaS wins by underwriting on operational data you already own. Here's how a platform out-underwrites cash-advance lenders.

By Mike Hodgen

Why generic cash-advance lenders underwrite half-blind

If you've ever watched a merchant cash advance get approved, you know the whole decision rests on one input: bank deposit history. That's it. The lender pulls three to six months of bank statements, looks at the average daily balance and the deposit cadence, and prices the advance off that. The entire model for embedded lending in vertical SaaS starts from the same place, and that's exactly where the opportunity hides.

A bank-data-only view is backward-looking and single-axis. It tells you what landed in the account. It tells you nothing about why.

One signal: bank deposits

A generic revenue-based financing provider can't see whether deposits are lumpy because of seasonality or because the business is dying. It can't tell whether a contractor just signed a quarter's worth of new work or just lost their biggest customer. It can't see whether deposits are being skimmed before they ever hit the account.

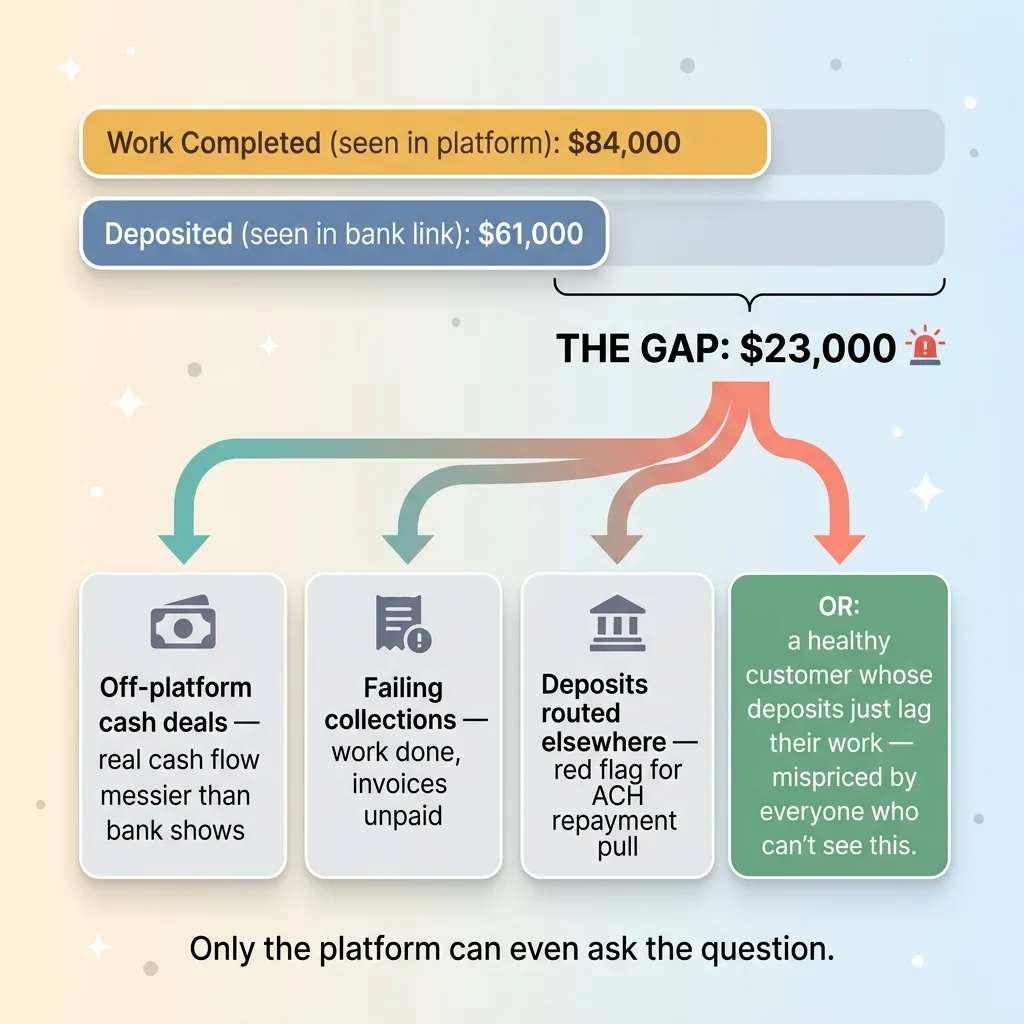

Here's the number that makes the point. Say a contractor completed $84,000 of installed jobs last month but only deposited $61,000. A generic lender sees $61,000 and stops there. That's the ceiling of what they know.

What trailing revenue can't tell you

This isn't a knock on any one lender. It's the structural limitation every standalone lender shares. They underwrite to trailing revenue because trailing revenue is the only signal they have access to.

And here's the doubt I'd have if I were a software CEO reading this: a SaaS company can't out-bank the banks on bank data alone. You're right. You can't. The edge isn't beating them at their own signal. The edge is having a second, richer signal they will never have. That's the whole game, and most vertical platforms are already sitting on it.

The data your platform already owns is the moat

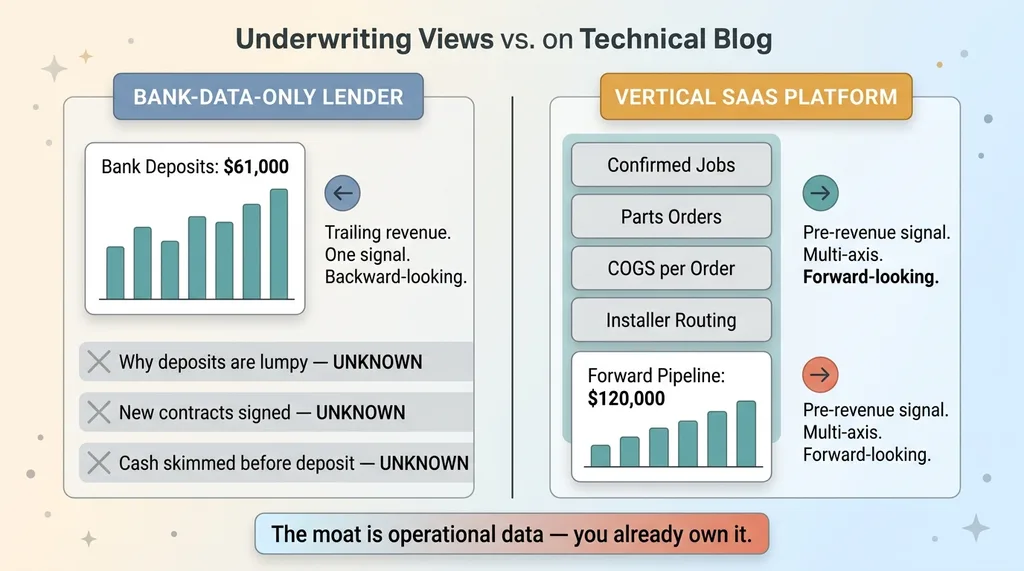

Picture a vertical ops platform for the window treatments trade. Quotes, scheduled jobs, parts orders, installer routing, cost of goods on every order. All of it flows through the software because that's what the software does.

Bank-data-only vs platform data underwriting view

Bank-data-only vs platform data underwriting view

That platform sees every customer's pipeline before a single dollar deposits. That is pre-revenue signal. That is the thing a bank will never have.

Jobs, orders, and COGS as underwriting signals

When a contractor has $120,000 of confirmed, scheduled, materials-ordered jobs on the calendar for next month, the platform can see it. The cash hasn't landed yet. The bank statement won't reflect it for 30 to 60 days. But the work is real, booked, and visible inside the product.

You can underwrite against that. You can lend against a confirmed pipeline of installed jobs before the money clears the account. That's the difference between a trailing-revenue view and a forward-pipeline view.

Underwriting to future pipeline, not trailing revenue

This is precisely the edge Shopify Capital has. Shopify sees GMV flowing through checkout before the deposit settles, so they can offer capital a bank-only lender would have to decline or overprice. Now transplant that exact mechanic to any vertical with operational data running through it.

The strategic point: this is capital as a feature, not a separate lending business. The fintech moat isn't access to capital. Capital is a commodity. The moat is operational data, and you already own it.

But the lending product is the last layer, not the first. It only works because the boring operational plumbing already exists, the scheduling, the order tracking, the COGS data. I've written before that AI is the last thing you build, not the first, and capital is the same. You earn the right to lend by owning the operational data first.

The fraud signal no standalone lender has

Back to that contractor who did $84,000 of work but only deposited $61,000. A generic lender sees the bank side and nothing else. A vertical platform sees both sides, and the gap between them is the most valuable underwriting signal in the entire stack.

Cross-referencing jobs done against deposits made

The platform knows $84,000 of work got completed because the jobs were marked done in the software. The bank link shows $61,000 deposited. So where's the other $23,000?

The jobs-done vs deposits-made gap as fraud and health signal

The jobs-done vs deposits-made gap as fraud and health signal

There are three different risk stories hiding in that gap. Cash deals done off-platform, which means the borrower's real cash flow is messier than the bank shows. A failing collections process, where work got done but invoices aren't getting paid. Or deposits routed to a separate account, which is a flashing red light if you're about to set up an ACH repayment pull against the account you can see.

Only the platform can even ask the question. A bank-data lender doesn't know $84,000 of work happened. They have no second number to compare against.

Why the gap is the alarm

And this cuts both ways, which is what makes it powerful. The same delta that catches a fraud risk also surfaces a healthy customer whose deposits simply lag their work.

A contractor with strong booked pipeline but slow-paying customers looks weak to a bank-only lender. Their deposits are soft, so they get declined or overpriced. The platform sees the completed work, the confirmed orders, the real demand, and can extend capital that the generic lender left on the table. That's a good customer mispriced by everyone who can't see what you can.

The combined signal, MCA underwriting bank data plus your own operational data, is the whole edge. One side without the other is half-blind.

The build sequence: bank-link, memo, rails

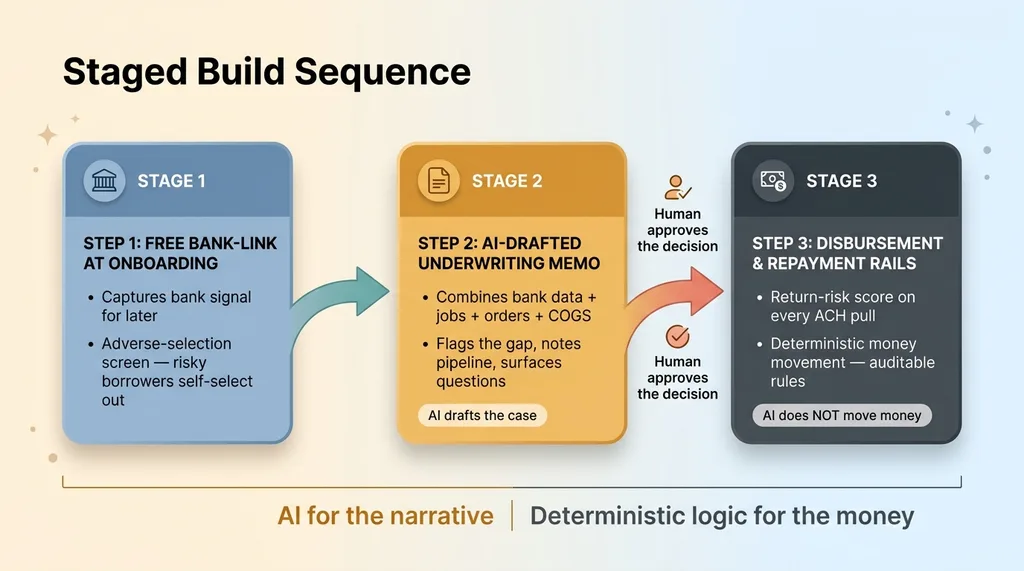

I want to be clear this is a strategy and a build plan, not a lender I've shipped to production. But the sequence matters, because the order is where most platforms would get this wrong. Here's how I'd stage it.

Three-step staged build sequence: bank-link, memo, rails

Three-step staged build sequence: bank-link, memo, rails

Free bank-link at onboarding doubles as an adverse-selection screen

Step one: a free bank-link at customer onboarding, before anyone borrows a dollar. This does two jobs at once.

It gives you the bank signal you'll need later. And it screens who you even let onto the platform. Customers who refuse to link their bank, or whose bank data flatly contradicts their stated business, self-select out before they ever become a lending risk.

That's adverse selection working in your favor at the front door instead of biting you after you've already advanced funds. The riskiest borrowers tend to be the ones who don't want you looking. Letting them opt out early is a feature, not a friction point.

AI-drafted underwriting memo

Step two: an AI-drafted underwriting memo. This combines the bank data with the platform's own jobs, orders, and COGS history into a single decision document.

The AI pulls the trailing deposit pattern, the forward pipeline, the jobs-versus-deposits delta, the seasonality, and writes a clean memo a human can read in two minutes. It flags the $23,000 gap. It notes the booked pipeline. It surfaces the questions.

Then a human approves the decision. The AI drafts the case. It does not set the number.

Disbursement and repayment rails

Step three: disbursement and repayment rails with return-risk scoring on every single ACH pull. Before you initiate a debit, you score whether it's likely to bounce, based on balance patterns and timing.

This is where I draw a hard line. The money-moving math stays deterministic. I've written a whole piece on why I make risk management deterministic, and lending rails are the textbook case. The AI drafts the memo. It does not decide the loan amount, and it absolutely does not pull the funds. Disbursement, repayment scheduling, and return scoring run on rules you can read, audit, and defend. A language model has no business deciding when to debit someone's bank account.

That separation, AI for the narrative, deterministic logic for the money, is what keeps this safe enough to actually run.

How to add capital without becoming a bank

Here's the doubt I promised to answer. You're a software company. You don't have a banking charter, a balance sheet to lend off, or a 40-person compliance department. Good. You don't need any of that.

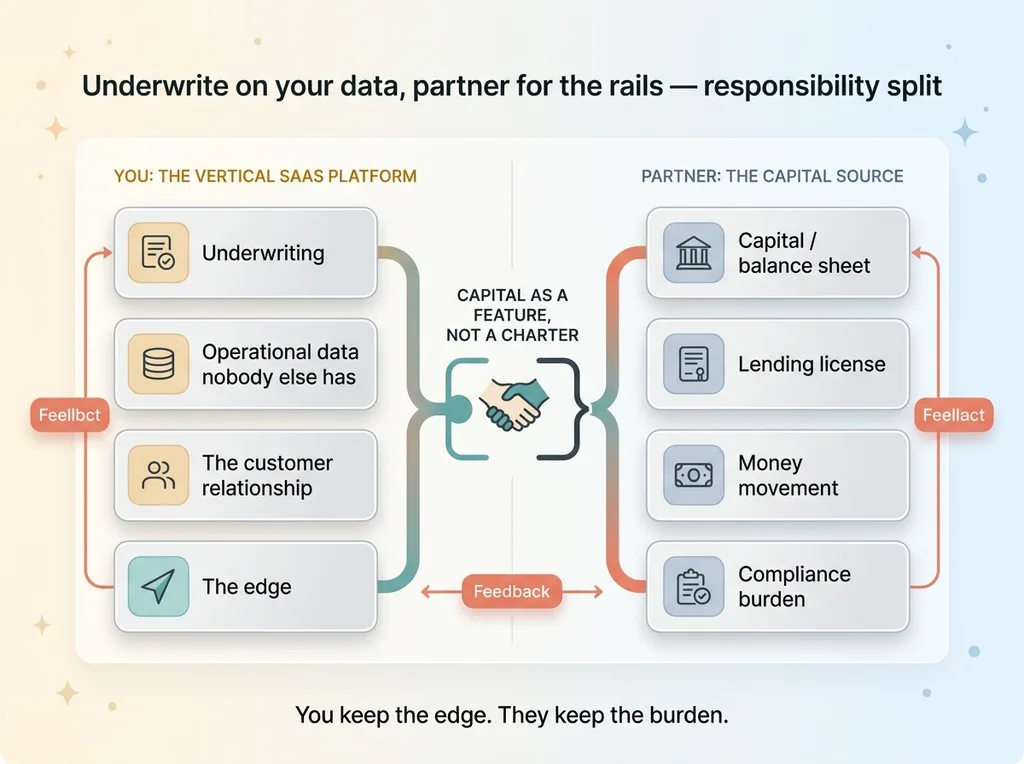

Underwrite on your data, partner for the rails

The split is clean. You own the underwriting, because you own the data nobody else has. You partner for everything regulated: the capital source, the lending license, the money movement, the compliance burden.

Underwrite on your data, partner for the rails, responsibility split

Underwrite on your data, partner for the rails, responsibility split

You contribute the one thing a bank can't replicate, the operational data on your own customers. The capital partner contributes the one thing you don't want, the regulatory and balance-sheet weight. Both sides bring what the other structurally can't.

This architecture isn't theoretical. The same model an e-commerce finance SaaS uses to offer revenue based financing software is fully transplantable to a trades platform, a field-services platform, a logistics platform. Any vertical where real operational data flows through the product. The data is different. The structure is identical.

Capital as a feature, not a charter

Frame this correctly for your board. You're not becoming a lender. You're adding a feature.

A capital feature raises retention, because customers don't churn off a tool that's also their line of credit. It increases platform stickiness, because financing makes your software load-bearing in their business. And it creates a real revenue line, all without taking on bank-grade risk your company was never built to hold.

Capital as a feature means the lending is a layer on top of the platform, underwritten by your data, powered by a partner's rails. You keep the edge. They keep the burden.

What this is worth and where it goes wrong

Let me give you both sides, because the honest version builds more trust than the pitch.

The retention and revenue case vs the honest failure modes

The retention and revenue case vs the honest failure modes

The retention and revenue case

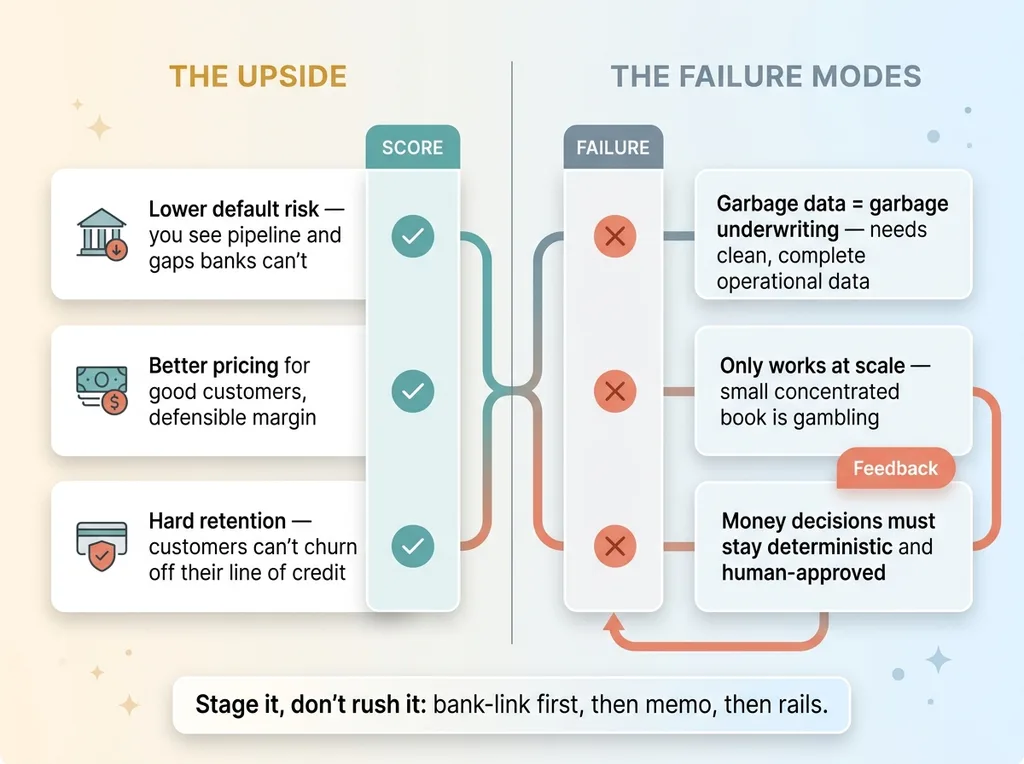

A capital product underwritten on proprietary operational data carries lower default risk than a bank-data-only competitor. You can see the booked pipeline they can't, and you can catch the deposit gaps they can't. Lower default risk means you can offer better pricing to good customers and still hold a defensible margin.

It also locks customers in hard. It's annoying to switch software. It's genuinely difficult to switch software that's also your active line of credit. That's retention you can't buy with features alone.

The honest failure modes

Now the limits, and they're real.

This only works if your operational data is clean and complete. If jobs get marked done inconsistently, if COGS is half-entered, if orders live in three systems, then you're underwriting on garbage and garbage underwriting loses money fast. The moat is only as good as the data hygiene underneath it.

It only works at scale. You need a customer base large enough that the loan book is diversified, so a few defaults don't sink the program. A small book with concentrated risk is just gambling with extra steps.

And you must keep the money-moving decisions deterministic and human-approved. The AI is for the memo, not the disbursement. I'll repeat that because it's the line people get wrong when they're excited.

This is a strategy you stage, not a feature you rush. Don't launch a lender in month one. Build the bank-link first, prove the data quality, then add the memo, then add the rails. In order.

Turning your operational data into a capital product

Most vertical SaaS companies are sitting on an underwriting edge they've never monetized. The data is already flowing through the product. The pipeline is already visible. The jobs-versus-deposits signal is already there, unused.

The question isn't whether you have the moat. If real operational data runs through your platform, you have it. The question is whether you've built the three pieces that turn it into a product: the bank-link at onboarding, the AI-drafted memo engine, and the return-risk-scored rails with deterministic money movement.

I build these systems, I don't just diagram them on a slide. That distinction matters here more than almost anywhere, because the gap between a lending strategy and a lending product is entirely in the rails. I've written about why I build these systems, not just advise on them, and embedded lending is exactly the kind of thing where shipping it is the only thing that counts.

If you run a vertical platform and you're wondering whether a capital feature makes sense, I'm happy to map it with you. What data you already have, what's clean enough to underwrite on, and what a staged build would actually look like. No hard sell. Just a clear picture of whether the moat you already own is worth turning into a product.

Thinking about AI for your business?

If this resonated, let's have a conversation. I do free 30-minute discovery calls where we look at your operations and identify where AI could actually move the needle.

Get AI insights for business leaders

Practical AI strategy from someone who built the systems — not just studied them. No spam, no fluff.

Hodgen.AI

Ready to automate your growth?

Book a free 30-minute strategy call with Hodgen.AI.

Book a Strategy Call