Accounting Data Migration Errors: When $0 Variance Lies

Why hitting zero variance against your old accounting system is a red flag, not a win. How I caught $48K in accounting data migration errors.

By Mike Hodgen

The Validation Number That Should Have Scared Me

I was rebuilding the books for a DTC fashion brand I run, migrating off a legacy accounting setup into a new ledger. I'd written the migration script, run it against years of transactions, and pulled up the validation report.

$0 variance. Penny-perfect against the old system.

Most people ship that and crack a beer. The numbers matched. The migration "worked." I almost did exactly that.

Then I asked the question that ruins your afternoon: what if the old numbers were wrong?

Because here's the thing nobody tells you about accounting data migration errors. If your new system matches the old one to the penny, all you've proven is that your new system faithfully reproduces whatever the old one did. Every category. Every total. Every mistake.

Zero variance felt like a green light. It was actually a warning sign I almost ignored.

The legacy system was the thing I was replacing. Often you replace a system precisely because nobody fully trusts it anymore. So why was I treating it as the gold standard for whether my new books were correct?

A balanced ledger can be confidently, completely wrong. It can sit there reconciling cleanly while overstating your cash by tens of thousands of dollars. I know because that's exactly what mine was doing.

The $0 variance wasn't proof of success. It was proof that I'd built an extremely efficient machine for copying errors forward.

I spent the next two days tearing the validation apart instead of celebrating it. What I found cost me a weekend and saved me from making decisions on money that didn't exist.

Let me walk you through it, because if you're moving off legacy software or letting AI clean up your books, this is the trap waiting for you.

Why Reconciling to the Old System Launders Its Errors

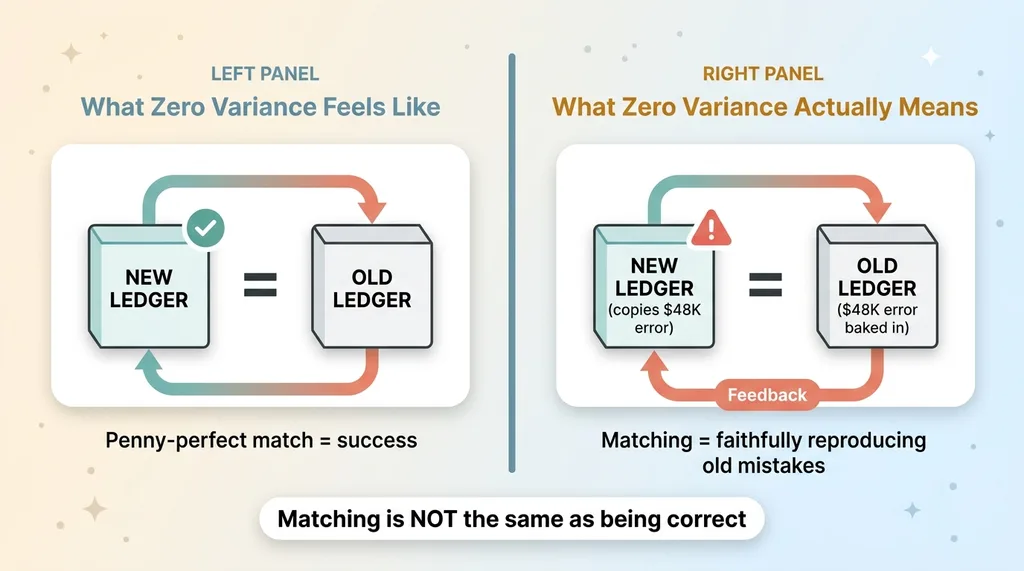

Zero variance is the bug, not the green light

Zero variance is the bug, not the green light

The hidden assumption in "zero variance"

When you validate a migration by reconciling to the legacy system, you're making one massive unspoken assumption: that the legacy system is correct.

That's the whole game. "Zero variance" doesn't mean "my new books are right." It means "my new books agree with my old books." Those are not the same statement, and the gap between them is where the money hides.

You're treating the thing you're replacing as ground truth. But you're replacing it for a reason. Maybe it's slow, maybe it's a mess, maybe nobody's reconciled it properly in years. Whatever the reason, you don't trust it. So why anchor your validation to it?

Matching is not the same as being correct

Here's the mechanical reality. If your legacy system has a $48K overstatement baked in, and your migration matches it perfectly, your shiny new system now has the same $48K overstatement. And it passed validation with flying colors.

The validation didn't catch the error. The validation guaranteed the error survived.

This is the single most common accounting data migration error I see, and it's not a coding bug. It's a logic bug. People pick the wrong reconciliation target.

The fix isn't a better script. It's a different anchor. You do not validate a system against the thing you're replacing. You validate it against something external and authoritative, something that doesn't share the old system's mistakes.

For accounting, that authority is sitting right there: the bank. Money either moved or it didn't. The bank doesn't care how your old software categorized things. It just records what actually happened.

That distinction (external authority versus internal agreement) is the whole ballgame. Get it wrong and you'll reconcile yourself straight into a problem.

What I Actually Found: $48,795 of Phantom Cash

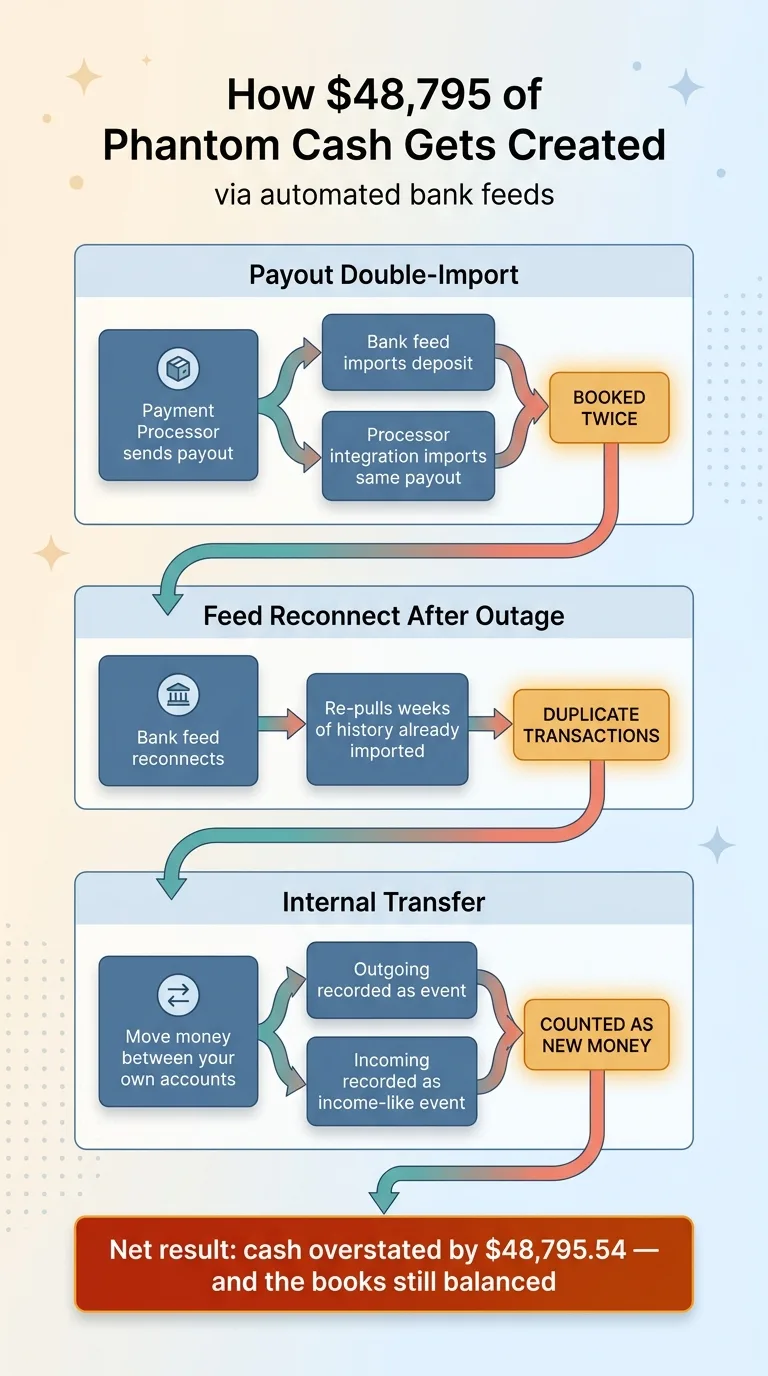

Duplicated transfers and payout double-imports

Once I stopped trusting the old totals, the picture got ugly fast.

How bank feeds create duplicate transactions

How bank feeds create duplicate transactions

The legacy bank feed had duplicated nearly every inter-account transfer and every payment-processor payout. Not once. Two and sometimes three times. The net result: cash overstated by $48,795.54.

Here's how that happens, because it's not exotic. It's the default failure mode of bank feeds.

A payment processor sends you a payout. It lands in your checking account as a deposit, and the bank feed imports it. Fine. But the processor integration also imports the same payout as its own transaction. Now you've booked it twice.

Reconnect a bank feed after an outage and it cheerfully re-pulls weeks of history you already have. Move money between two of your own accounts and a sloppy feed records both the outgoing transfer and the incoming one as separate income-like events. Every one of these is a textbook duplicate transactions accounting problem, and they're exactly the QuickBooks reconciliation errors that pile up quietly over years.

The month that looked $95K richer than it was

The duplicates weren't spread evenly. One month got hit especially hard, with income inflated by roughly $95,000.

Sit with that. An entire month looked like a blockbuster when a big chunk of it was the same dollars counted two and three times.

And here's the part that should make you nervous: the books balanced the whole time. Debits equaled credits. Every report tied out. The old system never once threw an error.

That's what makes this dangerous. A ledger that balances feels trustworthy. But "balanced" only means your double-entry is internally consistent. It says nothing about whether the underlying transactions are real. You can balance a ledger full of phantom money all day long.

The $0 migration variance had quietly carried all $48,795.54 of phantom cash into the new system. Penny-perfect.

Flipping the Source of Truth to Bank Statements

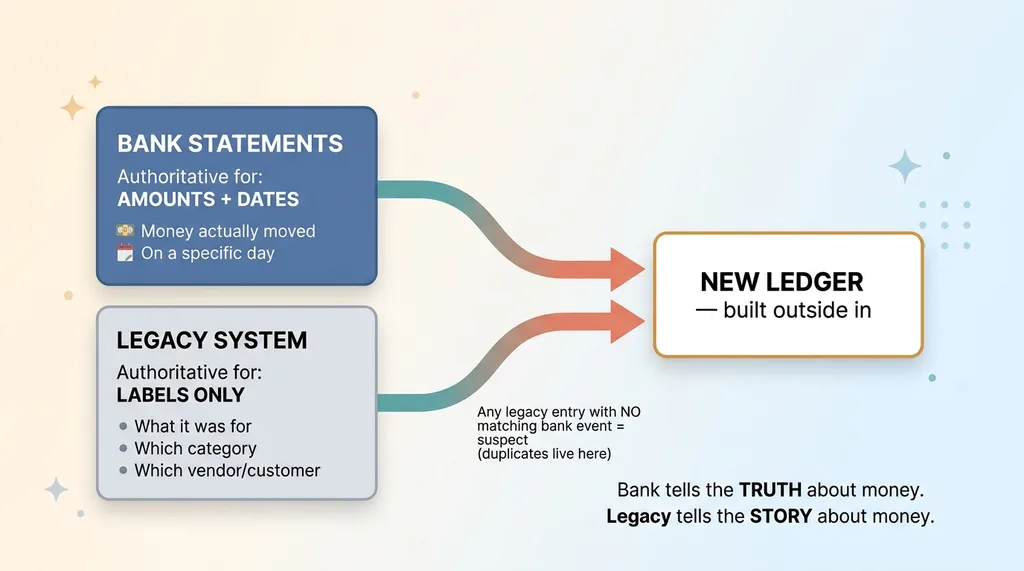

Bank gives amounts, old records give labels

The fix was to stop asking "does my new ledger match the old software" and start asking "does my new ledger match the bank."

Bank as authority for amounts, legacy as authority for labels

Bank as authority for amounts, legacy as authority for labels

I re-anchored the entire thing to bank statement reconciliation as the authority. This is the whole story of anchoring books to the bank, not the legacy software, and it changed how I think about every migration since.

The principle is simple once you see it. Your bank exports are authoritative for two things: amounts and dates. Money actually moved, on a specific day, in a specific amount. The bank has no opinion and no bug. It just records reality.

Your old records are authoritative for one thing: labels. They tell you what each transaction was for, which category it belongs to, which customer or vendor it ties to.

So you merge the two. You don't trust them equally. The bank tells you the truth about money. The legacy system tells you the story about money. You take amounts and dates from one, labels from the other.

Rebuilding the ledger from the outside in

This flips the build order. Instead of importing the old ledger and hoping it's right, you start from the bank and work inward.

Every dollar in the new ledger has to trace back to a real bank movement. If money didn't move, there's no transaction. Full stop. Then, and only then, does each verified bank event get its label from the legacy data.

The kicker: anything in the legacy system with no matching bank event is immediately suspect. That's where the duplicates lived. They had no second bank deposit to back them, because the money only moved once. Anchoring to the bank made the phantoms visible because they had nothing real to attach to.

This also reframes what "validation" even means. It's not "matches old system." It's "matches the bank." One of those is a copy of your past mistakes. The other is the actual money.

The Wash-Pair Scan the Bank-Tie Can't Catch

Anchoring to the bank fixed most of it. Not all of it. And the honest version of this story includes what the bank-tie misses.

Some double-counts net out at the bank level. They show up as offsetting pairs that look completely legitimate: a deposit and a matching reversal, a transfer in and a transfer out, a charge and a refund. Both transactions tie to real bank events. Both are individually defensible.

But sometimes only one of them should be booked, or the pair represents a duplicate that happens to cancel itself out in the totals.

A pure bank-tie won't flag these. The totals still reconcile. The sum is correct even when the individual transactions are wrong. Your primary reconciliation looks clean while a pile of garbage transactions sits inside it, balancing each other out.

So I ran a separate scan looking specifically for wash pairs and reversals: transactions that cancel each other and shouldn't both exist in the ledger. As I learned the hard way, a bank-tie alone won't catch wash pairs. It's a genuinely different class of problem and it needs its own check.

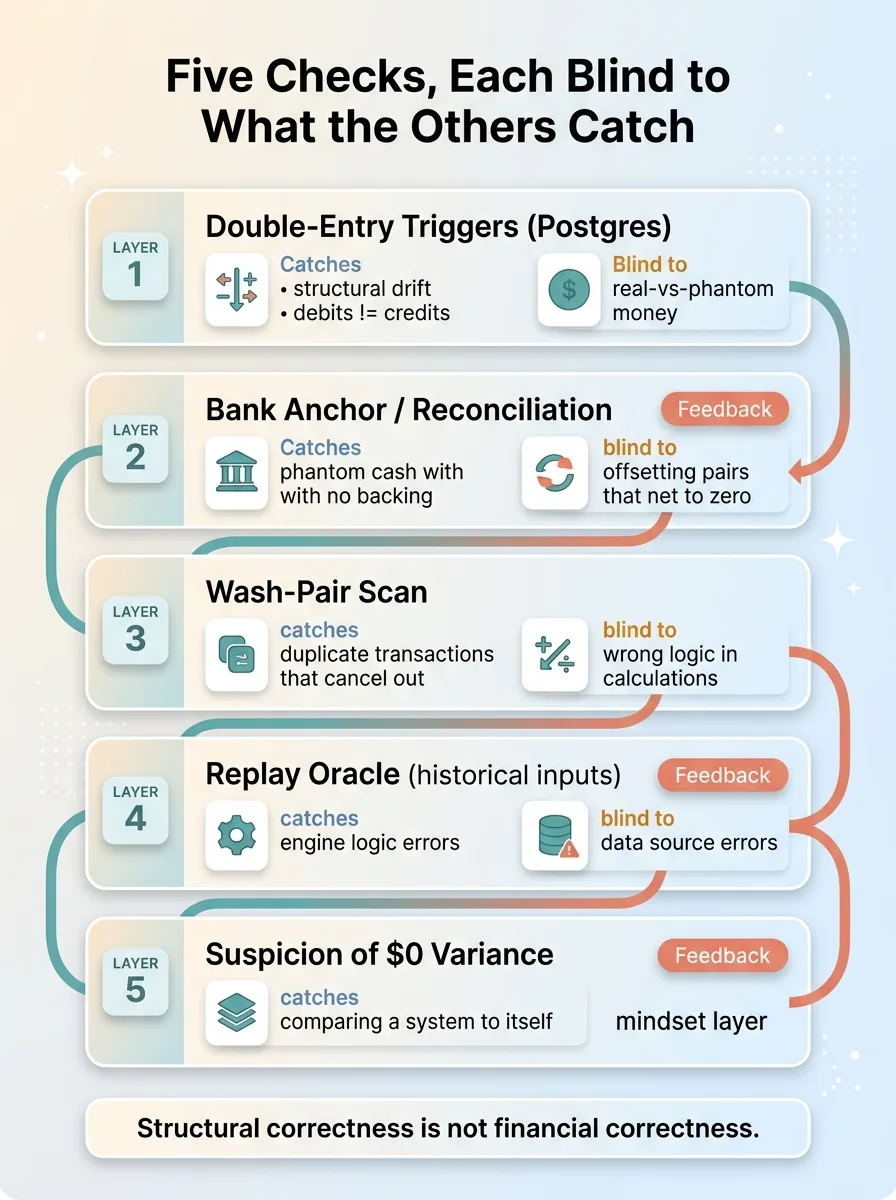

This is the part I want you to take seriously. No single validation is sufficient. The bank-tie catches phantom cash that has no backing. The wash-pair scan catches duplicate noise that nets to zero. Neither one catches what the other catches.

If you walk away thinking "great, I'll just reconcile to the bank and I'm safe," you'll miss this entire category. You need layered verification, where each layer is designed to catch what the previous one is structurally blind to.

That's not paranoia. That's just understanding that every check has a blind spot, and the only fix for a blind spot is a second check looking from a different angle.

How to Validate a Migration Without Laundering the Past

Here's the transferable version, whether you're moving off old software or letting AI clean up your books.

Anchor to external ground truth, not the legacy system

1. Pick an external authority as your reconciliation target. For accounting, that's bank statements, processor settlement reports, or tax filings. Not the old software. The authority has to be something that doesn't share your legacy system's mistakes.

2. Treat the legacy system as a source of labels, not amounts. This is the source of truth data decision that fixes the whole problem. The old records tell you what money was for. The external authority tells you what actually moved. Merge them, don't trust them equally.

3. Run independent scans for duplicates and wash pairs. Your primary reconciliation can't see offsetting pairs that net to zero. Build a separate check for them.

4. Be deeply suspicious of $0 variance. When a migration matches the old system perfectly, the most likely explanation isn't that you nailed it. It's that you're comparing a system to itself. Real-world data has friction. Perfect agreement usually means you're measuring the wrong thing.

Validate the logic against history, not the data against itself

There's a second layer most people skip. So far we've talked about validating the data. But if your migration involves any engine (a pricing calculation, a tax computation, a categorization model, anything that transforms numbers), you also have to validate the logic.

Five layered validation checks each with a blind spot

Five layered validation checks each with a blind spot

The way to do that is to replay historical inputs through your new engine and check the outputs against known-correct results. This is what I mean by validating a financial engine against historical results: you don't check the engine against itself, you check it against outcomes you already know are right.

For my brand, the old software got replaced by a Postgres ledger I built with double-entry triggers. The triggers enforce that debits equal credits at the database level, so the structure can't drift. But structural correctness still isn't financial correctness. That's why the bank anchor, the wash-pair scan, and the replay all stack on top.

Five checks, each blind to something the others catch. That's what real validation looks like.

The Cost of Trusting a Number Because It Matched

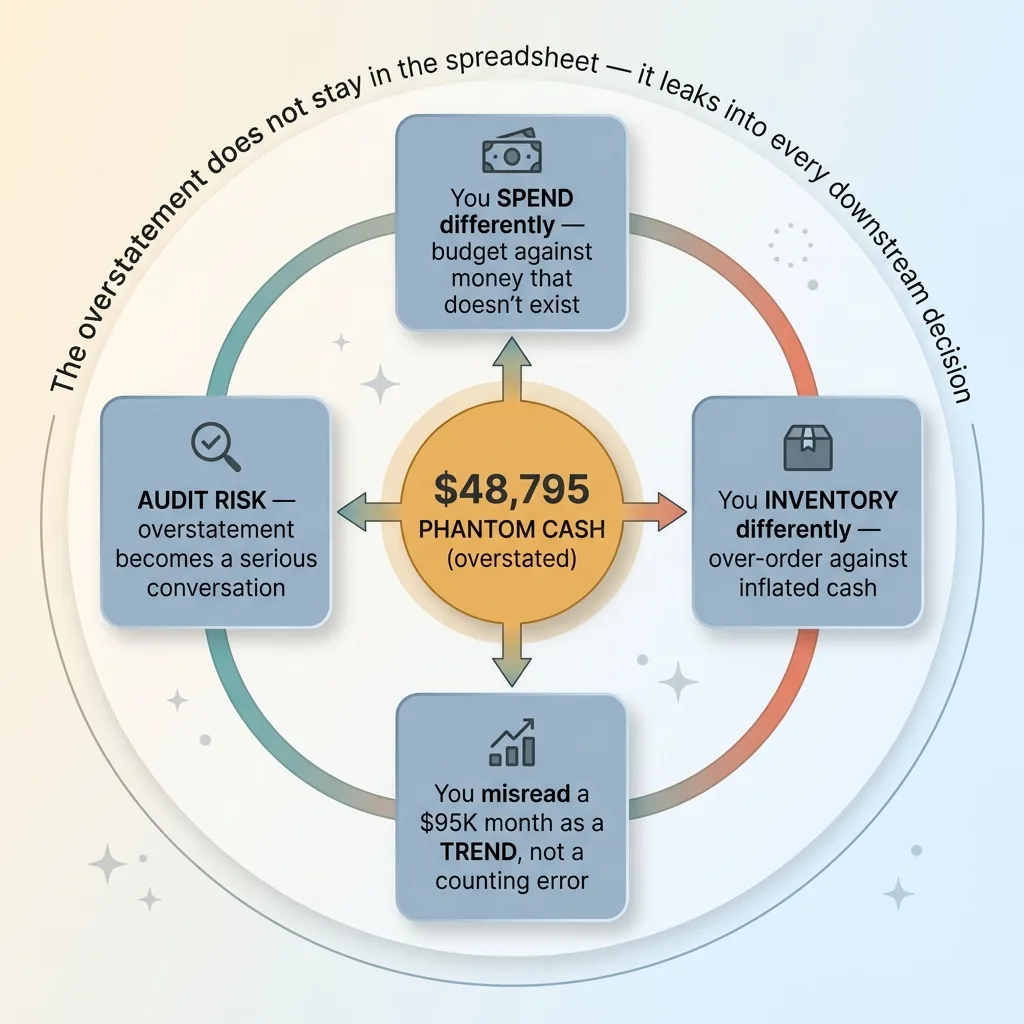

The $48,795 wasn't an accounting curiosity. It was decisions getting made on cash that didn't exist.

How phantom cash leaks into downstream business decisions

How phantom cash leaks into downstream business decisions

When you think you're sitting on more money than you are, you spend differently. You inventory differently. You read a $95K month as a trend instead of a counting error. The overstatement doesn't just live in a spreadsheet. It leaks into every choice downstream of it.

And in an audit or any formal financial review, an overstatement like that isn't a footnote. It's the difference between a clean process and a serious conversation you don't want to have.

Here's the broader point, and it applies to any business letting AI move fast on its data. Automation makes migrations and cleanups quick. But speed amplifies whatever your validation logic assumes. If your only check is "does the new thing match the old thing," you've built a very efficient machine for copying mistakes at scale.

The skill was never running the migration. The tooling for that is easy. The skill is knowing which number to trust, and refusing to trust the one you're replacing.

If you're moving off legacy systems, consolidating data, or pointing AI at your books to clean them up, the validation strategy matters more than the tooling. That's the part that's invisible until it bites you, and it's exactly where I'd want to bring in someone who's done this before you ship a migration that quietly carries your old errors into a brand-new system.

Want to explore what AI could do for your business?

Book a free 30-minute strategy call. No pitch deck, no sales team, just a real conversation about your operations and where AI actually fits.

Get AI insights for business leaders

Practical AI strategy from someone who built the systems — not just studied them. No spam, no fluff.

Hodgen.AI

Ready to automate your growth?

Book a free 30-minute strategy call with Hodgen.AI.

Book a Strategy Call