Bank Reconciliation Pitfalls: The Wash-Pair Trap

Your books can balance to the penny and still lie. The bank-tie only proves the net. Here are the bank reconciliation pitfalls a balanced ledger hides.

By Mike Hodgen

The Lie a Balanced Ledger Tells You

I was reconstructing a company's books from raw bank exports. Months of CSVs, thousands of lines, no clean accounting system to start from. I wrote the categorization rules, ran them, and tied the result back to the bank.

It balanced to the penny.

That feeling is dangerous. The bank-tie came out clean, and clean ties feel like done. Net inflows minus net outflows equaled the exact change in the bank's ledger. If you have ever stared at a reconciliation that finally zeroes out, you know the relief. You want to close the laptop.

I didn't close the laptop. And it's a good thing, because the balanced ledger was lying to me. Not about the total. About almost everything else.

Here is the thing most people miss about bank reconciliation pitfalls: a reconciliation that ties net inflows minus net outflows to the bank's balance change proves the net is right. That's it. It proves the net. It does not prove a single category label is correct.

This is the exact tension a CEO feels when they hear AI is going to categorize their transactions. If the machine sorts everything and the books still balance, how do you trust the labels? What does "reconciled" even certify?

I'll answer that in one line, and the rest of this article earns it: balancing only proves the net. Specific deterministic scans catch everything else.

Let me show you how a perfectly balanced ledger can be wrong in ways that quietly distort your taxes, your covenants, and your valuation.

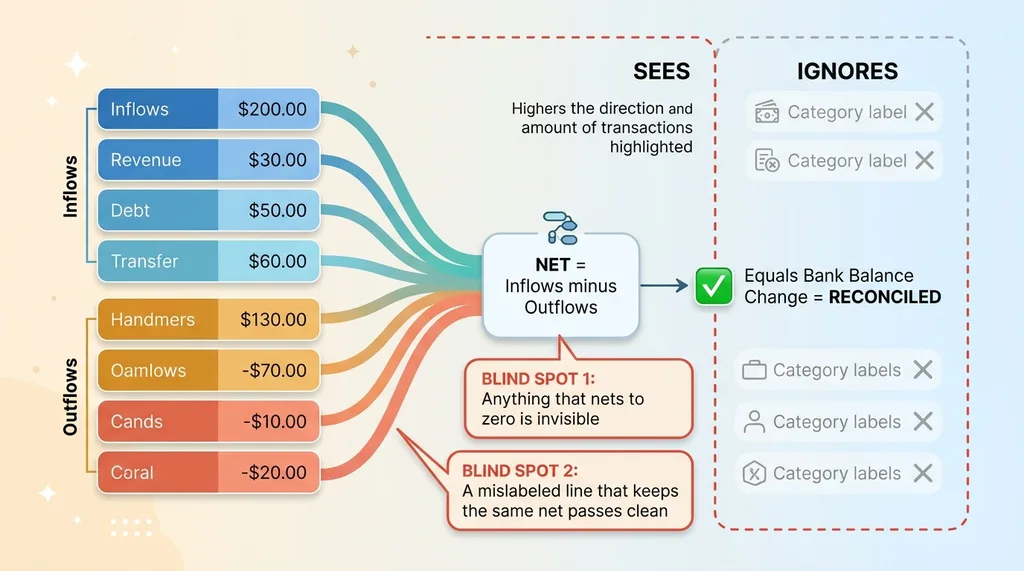

What a Bank-Tie Actually Proves (And What It Can't)

The math the reconciliation does

A bank reconciliation does one piece of arithmetic. It takes the sum of all inflows, subtracts the sum of all outflows, and confirms that number equals the bank's beginning-to-ending balance change.

That's the whole check. It operates at the net level.

Here is the part that trips people up. That arithmetic can be flawless while every individual label underneath it is wrong. The tie does not look at categories. It looks at direction and amount.

This is the heart of gross vs net reconciliation. The net tie sees money in and money out. It is blind to what the money was for.

The blind spots it leaves wide open

Two structural blind spots fall out of this immediately.

What a bank-tie proves vs what it can't see

What a bank-tie proves vs what it can't see

First, anything that nets to zero is invisible. A payment that comes in and bounces back out the same period contributes nothing to the net. The tie never sees it.

Second, any single mislabeled line that doesn't change the net total passes clean. If a transaction is an outflow and you label it the wrong kind of outflow, the net is identical. The tie doesn't blink.

Here's a concrete example:

| Transaction | True category | AI label | Direction | Nets correctly? | |---|---|---|---|---| | $6,936 disbursement | Tax payment | Bank fee | Outflow | Yes |

That $6,936 was a tax payment. My rules labeled it a bank fee. Both are outflows. The category is wrong. The total is right. The reconciliation ties.

So what does "reconciled" actually certify? It certifies the net. Nothing more. Treating a clean tie as proof that your categories are correct is the single most common reconciliation mistake I see, and it is the foundation of every problem below.

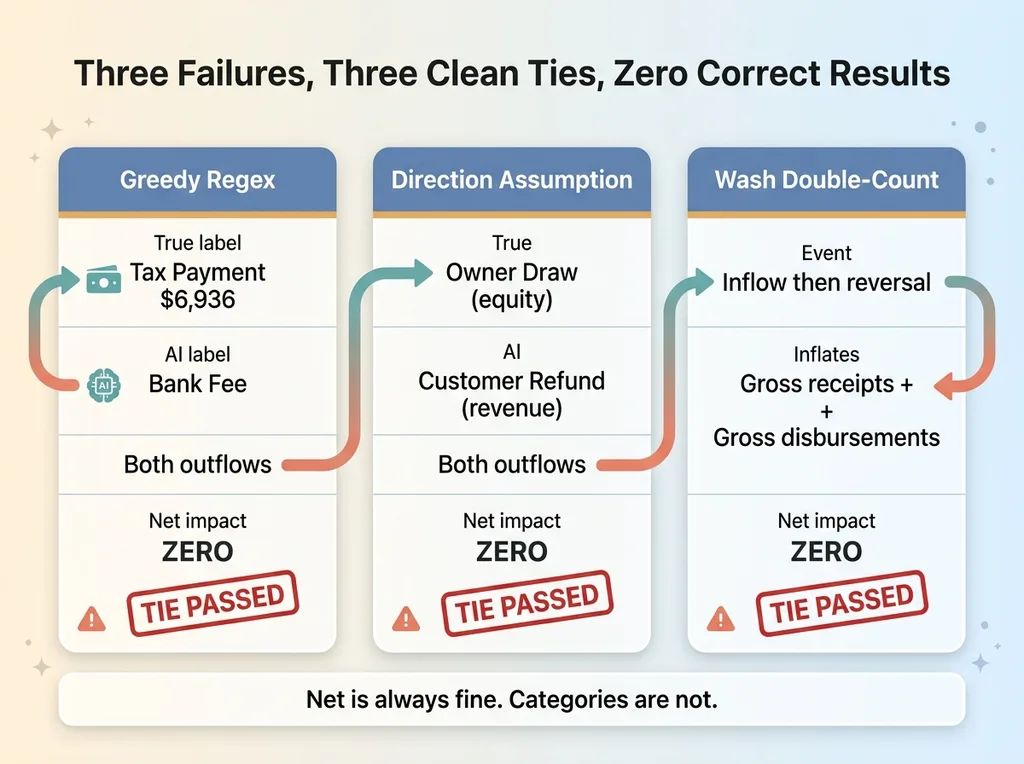

Three Categorization Failures the Tie Never Caught

Rebuilding those books, I ran my own label rules across thousands of transactions. Three failure modes got past the bank-tie completely. All three balanced. None were right.

Three categorization failures that passed the tie

Three categorization failures that passed the tie

Greedy regex: a $6,936 tax payment labeled a bank fee

I had a rule keyed on the string "FEE" to catch bank charges. Reasonable on its face. Bank fees almost always contain that word.

The problem is substring matching is greedy. A tax payment description happened to contain those three letters in sequence inside an unrelated word. The rule swallowed it. A $6,936 tax disbursement got filed as a bank fee.

Net impact on the tie: zero. Both are outflows. Impact on the books: a tax payment vanished from the tax line and inflated fees by nearly seven grand.

Direction assumption: an owner draw labeled a customer refund

The second failure was an assumption baked into a rule. It saw a transaction type and assumed customer refund. The actual transaction was an owner draw.

Both are outflows. The tie didn't care. But a refund reduces revenue, while an owner draw is an equity distribution. Two completely different lines on the financials, treated as identical because they pointed the same direction out of the account.

The wash double-count: a bounced payment inflating both sides

The third one is the dangerous one. A payment posted as an inflow, then bounced back out as a reversal.

The original inflated gross receipts. The reversal inflated gross disbursements. The two netted to exactly zero, so the bank-tie sailed right past it. Meanwhile gross revenue was overstated by the full payment amount and gross expenses by the same.

This is automated transaction categorization errors in the wild. And it is a reminder that AI is great at finding problems and terrible at being trusted without a layer underneath it. The model can sort a thousand transactions in seconds. It will also confidently mislabel the ones that look almost right. Speed without verification is just fast wrongness.

Three failures. Three clean ties. Zero correct results.

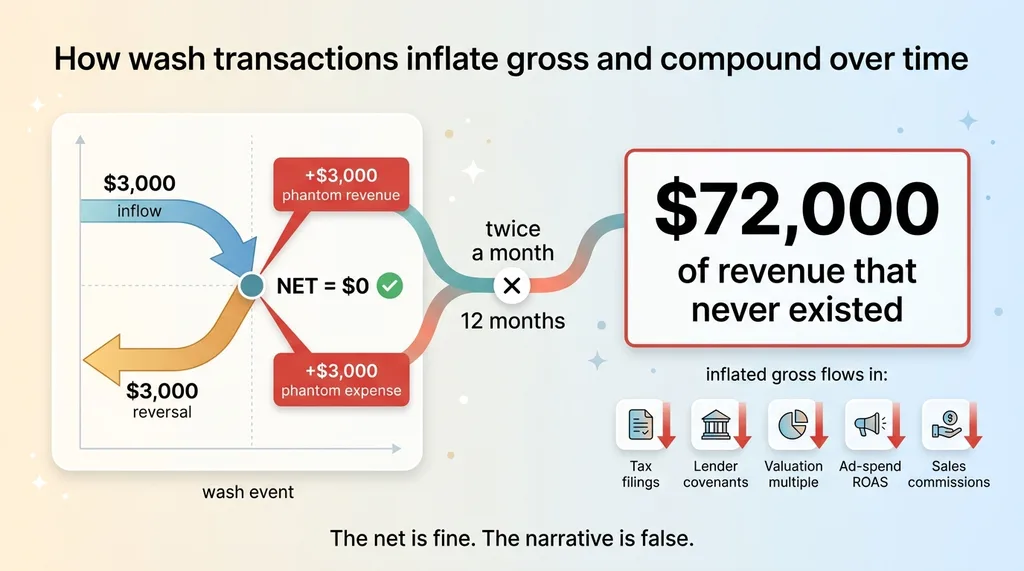

Why Wash Transactions Are the Most Dangerous Kind

Of those three, the wash pair is the one that keeps me up at night, and it should be the one your finance team scans for first.

How wash transactions inflate gross and compound over time

How wash transactions inflate gross and compound over time

A mislabel is at least visible if you read the line. Pull up the $6,936 entry, check the description, and you can catch it with your eyes. Tedious, but possible.

A wash pair is structurally invisible to the net tie and it inflates two numbers people actually report. Gross receipts and gross disbursements. Those are not internal-only figures. They leave the building.

Think about where gross revenue goes. It feeds tax filings. It feeds lender covenants. It feeds your valuation multiple when you raise or sell. It is the denominator in your ad-spend ROAS. It's the base for sales commissions.

An inflated gross from wash transactions quietly misstates every one of those while your books still balance.

Here's how it compounds. Say a customer payment of $3,000 bounces, posts, and reverses. That's $3,000 of phantom revenue and $3,000 of phantom expense in one event. Now imagine that happens twice a month across a year. That's $72,000 of revenue that never existed, sitting in your gross.

The net is fine. The net is always fine. That is exactly why nobody catches it. But the story your numbers tell, the story your lender and your buyer and the IRS are reading, is false.

Wash transactions accounting failures don't break the balance. They corrupt the narrative on top of a balance that looks perfect.

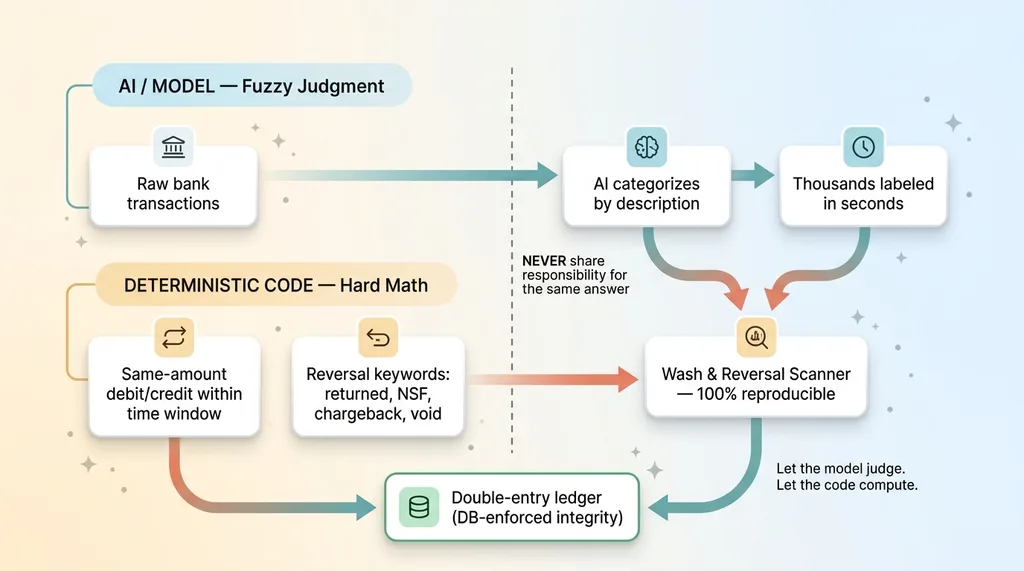

The Standalone Wash and Reversal Scanner I Built

So I built a separate scanner. Not part of the bank-tie. Independent of it. It runs every period as its own pass, because the net-level tie structurally cannot see gross inflation and never will.

What it keys on

The scanner looks for two signals.

The first is reversal keywords in the transaction description. Returned, reversal, NSF, chargeback, void, and a handful of others. Anything that signals a payment came back. These catch the washes that announce themselves.

The second signal catches the ones that don't. It scans for same-amount offsetting debit/credit pairs within a time window. A $3,000 inflow and a $3,000 outflow close together get flagged as a probable wash even when the description says nothing useful. Plenty of reversals carry no keyword at all, so the amount-matching is what closes the gap.

Why it has to be deterministic, not AI

This scanner is plain code. No model in the loop. That is deliberate.

AI labels, code audits - the separation of responsibilities

AI labels, code audits - the separation of responsibilities

The AI does the categorizing, because labeling thousands of transactions by description is exactly the kind of fuzzy pattern work models are good at. But the wash check is a hard arithmetic match, and it has to be 100% reproducible. It cannot hallucinate a pairing that isn't there, and it cannot miss one that is.

This is the principle I come back to constantly: let the model judge, let the code compute. Categorization is a judgment call. Matching a $3,000 debit to a $3,000 credit within seven days is not a judgment, it's math. You never hand math to a model that occasionally improvises.

The whole thing lived inside a larger project: rebuilding books on a ledger that can't be wrong. The ledger enforced double-entry integrity at the database level. The wash scanner sat on top of it as an independent audit. The model labels, the code audits, and the two never share responsibility for the same answer.

That separation is the entire point. AI for the fuzzy work. Deterministic scans for the verification. Mix them and you lose the one thing that makes the audit trustworthy: reproducibility.

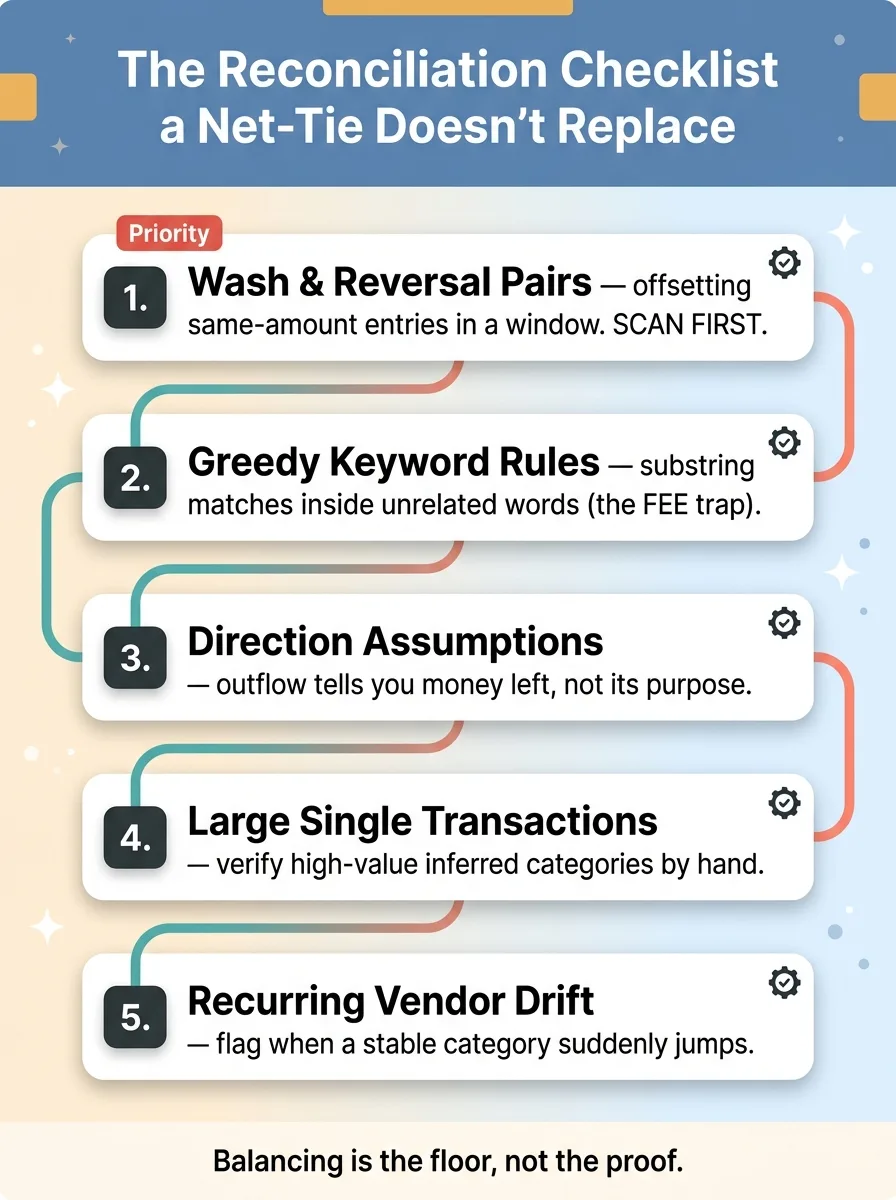

The Reconciliation Checklist a Net-Tie Doesn't Replace

Here is the portable version. These are the bank reconciliation pitfalls I scan for every period, every one of them as a deterministic check you can automate, none of them covered by the net-tie.

The five-item reconciliation checklist beyond the net-tie

The five-item reconciliation checklist beyond the net-tie

1. Wash and reversal pairs. Offsetting same-amount debit/credit entries within a window, plus reversal keywords. This is the invisible one. Scan for it first.

2. Greedy keyword rules. Any rule matching a substring inside a description. The "FEE" rule that ate a tax payment is the cautionary tale. Audit your match rules for substrings that appear inside unrelated words.

3. Direction assumptions. Any rule that labels an outflow's purpose without confirming it. Outflow direction tells you money left. It does not tell you whether it was a refund, a draw, or a payment. Flag categories that were assumed from direction alone.

4. Large single transactions with inferred categories. Any high-value line where the category came from a rule rather than a confirmed source. A wrong label on a $50 charge is noise. A wrong label on a $50,000 transfer moves your financials. Verify the big ones by hand.

5. Recurring vendors that suddenly change category. If a vendor was payroll for eleven months and reads as office supplies in month twelve, something broke. Track category stability across periods and flag the jumps.

That's the AI bookkeeping accuracy message in one list. Automated categorization is fine and fast. I use it constantly. But accuracy doesn't come from trusting the balance. It comes from layering independent verification on top of the balance.

Balancing Is the Floor, Not the Proof

A balanced ledger is necessary. It is nowhere near sufficient.

The companies that get burned are the ones that trust the balance and skip the verification layer. They see the tie zero out, they feel that relief I felt, and they close the laptop. Then the inflated gross shows up in a tax filing or a due-diligence review and it costs them something real.

The companies that don't get burned run independent deterministic scans every period. They treat the balance as the starting line, not the finish.

I've reconstructed books from raw bank data, and I've built the scanners that catch exactly what the tie hides. The wash detector, the greedy-rule audit, the direction-assumption flags. None of it is glamorous. All of it has saved real money.

And this lesson generalizes far past bookkeeping. Anywhere you put AI to work labeling data, whether it's transactions, support tickets, leads, or inventory, you need a separate deterministic check that proves the work is actually right. Not plausible. Right. That discipline of proving the work is actually right is what separates AI you can trust from AI that just looks confident.

If you're putting AI anywhere near your numbers and you want to know they're correct and not merely balanced, that verification layer is exactly what I build.

Want to explore what AI could do for your business?

Book a free 30-minute strategy call. No pitch deck, no sales team. Just a real conversation about your operations and where AI actually fits.

Get AI insights for business leaders

Practical AI strategy from someone who built the systems — not just studied them. No spam, no fluff.

Hodgen.AI

Ready to automate your growth?

Book a free 30-minute strategy call with Hodgen.AI.

Book a Strategy Call