AI Compliance Defense: Arm Experts to Push Back

Most AI compliance tools only flag violations. Here's how I built AI compliance defense that cites the exemptions protecting content that's actually fine.

By Mike Hodgen

The Real Friction Isn't Catching Violations

Most AI built for regulated industries is designed to find problems. It scans content, flags risk, and hands the compliance team a longer list of things to worry about. That's the default assumption about what AI compliance defense looks like: a smarter censor.

But when I worked with a financial advisory firm affiliated with a national broker-dealer, the bottleneck wasn't bad content. Every piece of public communication went through a home-office compliance team for review. And the problem wasn't that violations were slipping through.

The problem was that good content was getting killed.

The reviewers were over-applying rules. Content that should have shipped in a day got stuck in back-and-forth for a week or more. An advisor would write something genuinely compliant, the reviewer would flag a vague concern, the advisor would revise, the reviewer would flag something else, and around it went.

By the time anything cleared, the moment had passed. The firm's publishing cadence was effectively dead.

Here's the part that surprised me. The advisor wasn't wrong. And the reviewer wasn't wrong either. The reviewer was being safe, not accurate. Those are different things, and the gap between them was costing the firm real market presence.

So I stopped thinking about AI as a tool to catch more violations. The firm didn't have a violation problem. It had a friction problem. The more valuable move was the opposite of a censor: a tool that could defend compliant content instead of just flagging risky content.

That single inversion changed everything about how I built for them. Instead of arming the compliance team with more reasons to say no, I armed the advisor with the ammunition to win the argument when the answer should have been yes.

Let me explain why that distinction matters more than it sounds.

Why Over-Caution Is More Expensive Than You Think

The hidden tax on every piece of content

Nobody books over-caution as a line item. There's no invoice for the content that never shipped. That's exactly why it's so expensive: it's a cost the firm pays constantly and never measures.

Think about the math. If a firm could realistically ship three to four pieces of content a week, but compliance friction grinds that down to one, that's a 70%-plus reduction in market presence. Your competitors are publishing freely while your firm goes quiet. Nobody in the building can point to the dollar figure, but the lost ground is real.

And it compounds. An advisor with genuine expertise gets a few pieces killed, learns that proposing content is a losing battle, and stops proposing. The firm's best voices go silent, not because they're prevented from speaking but because the friction taught them not to bother.

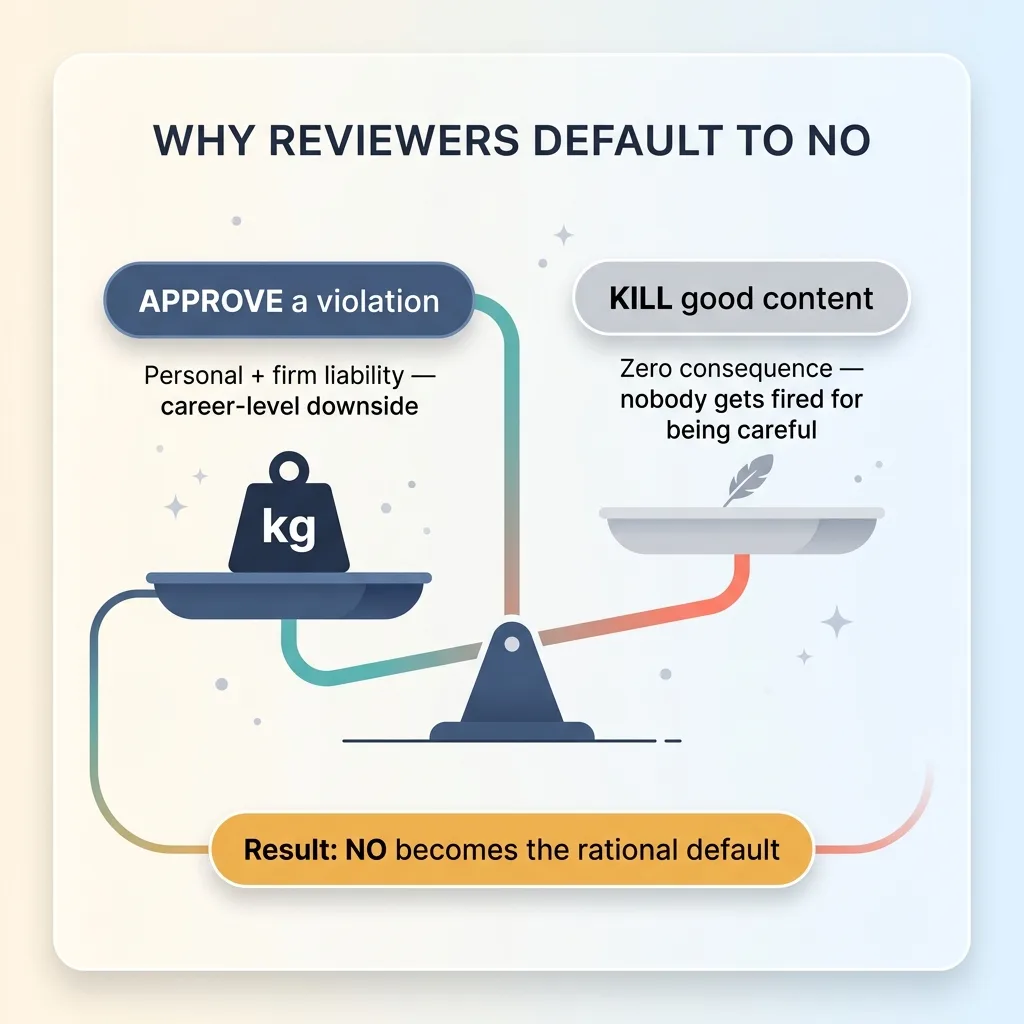

Why reviewers default to no

The reason this happens is pure incentive math. A home-office reviewer carries personal and firm liability if they approve something that turns out to violate a rule. That's a career-level downside.

The Broken Incentive Asymmetry

The Broken Incentive Asymmetry

If they kill content that was actually fine? Zero consequence. Nobody gets fired for being too careful.

That asymmetry makes "no" the rational default. When approving has real downside and rejecting has none, a busy reviewer is going to reject anything that gives them the slightest pause. It's not laziness. It's the only sane response to broken incentives.

I want to be clear here: the reviewers aren't the villains. They're under-resourced, reviewing a high volume of content, and operating in a system that punishes one type of mistake and ignores the other. Given those constraints, over-caution is the correct individual choice. It's just terrible for the firm as a whole.

That's the real cost of compliance friction. It's not the occasional violation. It's the steady, invisible erosion of everything your firm could have said but didn't.

What a Regulatory Defense Brief Actually Does

Censor vs Advocate: The Inversion

Censor vs Advocate: The Inversion

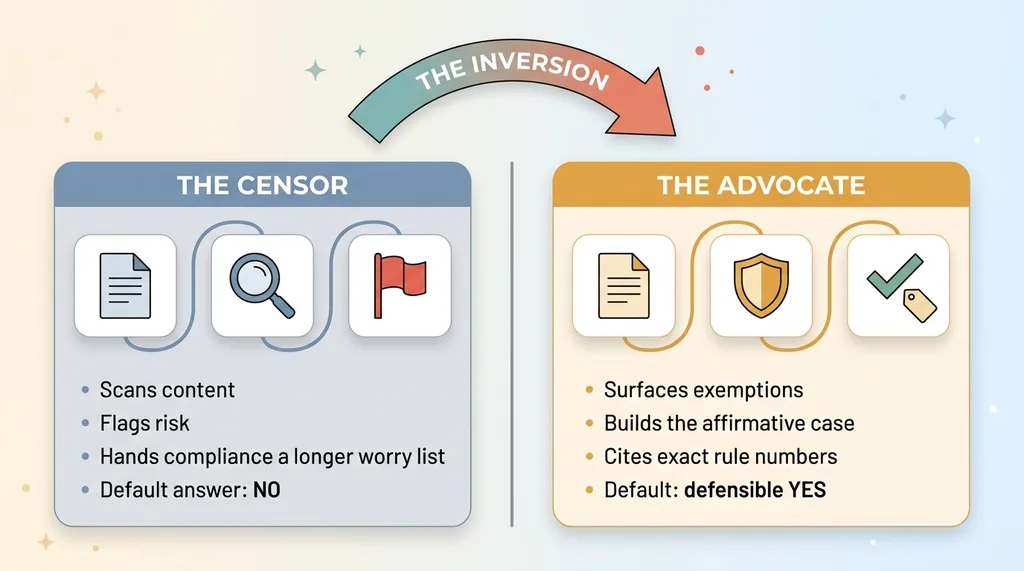

From censor to advocate

I already had a content auditor running for this firm. It did the normal thing: scanned content and flagged genuine violations. Useful, but it was still playing on the censor's side of the table.

So I added a second mode. I called it a regulatory defense brief.

For each piece of content that's actually compliant, the model surfaces the specific exemptions that protect it. Not a general "this looks okay." It builds the affirmative case for why the content is allowed, citing the exact rules that make it allowed.

That's the shift. The same underlying engine that catches problems now also defends the content that doesn't have any. It went from being the firm's censor to being the advisor's advocate.

An example: the public-appearance exemption

Here's how it works in practice, anonymized.

Anatomy of a Regulatory Defense Brief

Anatomy of a Regulatory Defense Brief

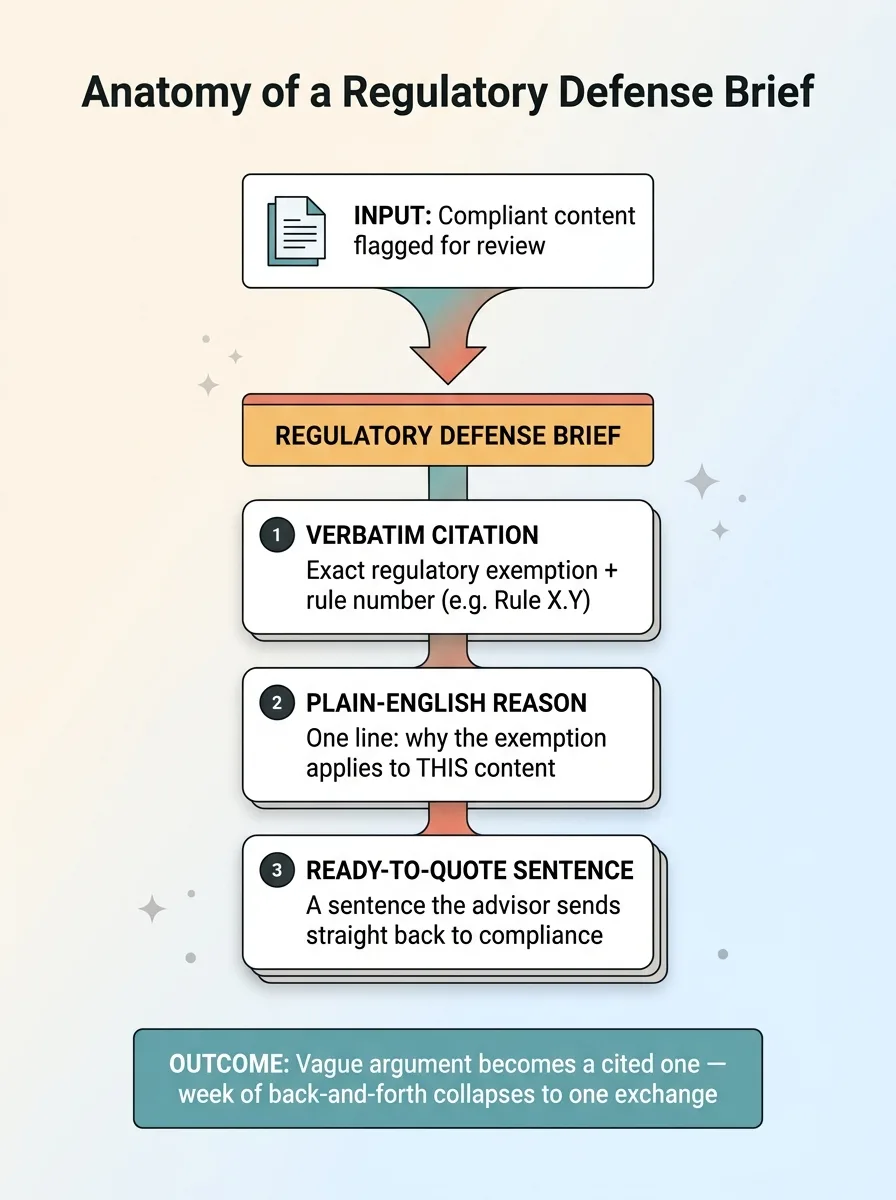

An advisor writes a piece of content that qualifies under a public-appearance exemption from pre-use approval. A reviewer, defaulting to caution, flags it for full review anyway. Normally that kicks off a week of back-and-forth.

Instead, the defense brief returns three things. The verbatim regulatory exemption citation, the actual rule number. A one-line plain-English explanation of why the exemption applies to this specific content. And a ready-to-quote sentence the advisor can send straight back to compliance.

The format is the whole point. It's not "this is probably fine." It's "this is protected under rule X.Y because Z, and here is the exact sentence to send your reviewer."

That turns a vague argument into a cited one. The advisor stops saying "I think this is okay" and starts saying "this is covered under this specific exemption, here's the rule." Those two conversations go very differently.

This is what AI for regulated marketing should actually do: not just police your content, but know the rulebook well enough to defend it.

Answering the Real Fear: Won't AI Make Compliance Even More Paranoid?

The instinct most people have is reasonable. If you point an AI at your content and it starts flagging more issues, won't that just make the compliance team slower and more anxious? More flags, more fear, more delays.

That's true if the AI only flags. A tool that does nothing but surface risk really does make everyone more paranoid. It hands the reviewer a longer worry list and gives them more reasons to say no.

But the defense brief does the opposite, and here's why.

Reviewers say no because saying yes is scary and undocumented. They're approving something on instinct, with their own liability on the line, and nothing on paper to back them up if it goes wrong. Of course they hesitate.

A defense brief gives them the documentation. When the advisor walks in with the specific exemption cited, verbatim, the reviewer now has a defensible, documented reason to approve. The paper trail that protects the advisor's content also protects the reviewer who signs off on it.

So the tool reduces friction on both sides. The advisor stops losing arguments they should win. The reviewer gets the cover they need to feel safe saying yes. Both parties are better off, which almost never happens when you just add another flagging layer.

There's one non-negotiable condition for this to work: the citations have to be real. A hallucinated rule number would destroy trust the first time a reviewer looked it up and found nothing. The entire value of the brief is that the reviewer can verify it.

That's why the system is grounded against the actual rulebook, not the model's memory. Which brings me to the guardrail that makes all of this safe.

Why the AI Advocates But Never Decides

The line I won't cross

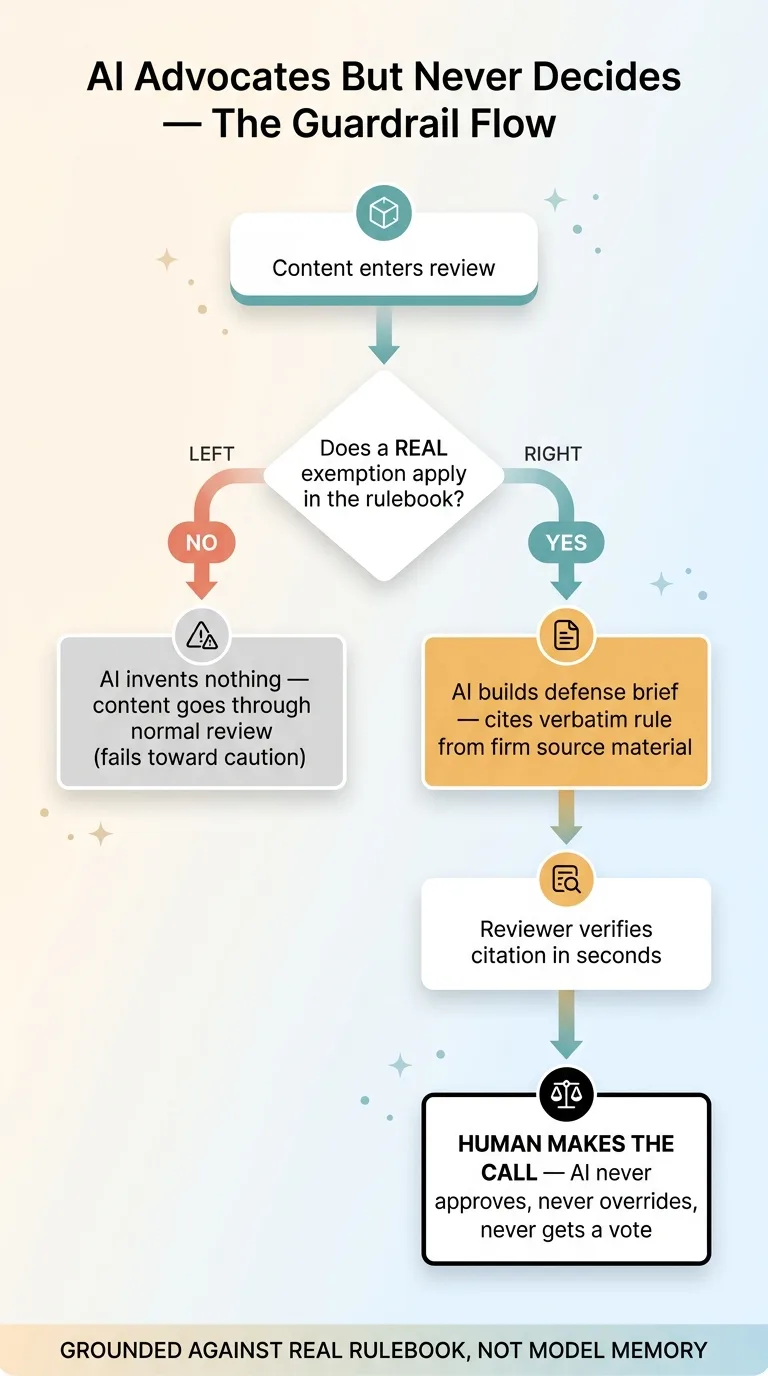

The AI does not approve content. It does not override compliance. It does not get a vote.

It builds the case and hands it to a human who makes the call. That's the line, and I don't cross it. The reviewer is still the decision-maker. The advisor is still responsible for what they publish. The AI is just the researcher that found the relevant exemption faster than a human could.

This is the same principle behind every AI system I ship stops for a human. The model is in service of the expert, never in the driver's seat. In a regulated context, that isn't a nice-to-have. It's the only design that doesn't eventually blow up in your face.

Grounding citations so they hold up

The model is constrained to cite from the firm's actual regulatory source material, with verbatim rule text. A reviewer can verify every line in seconds because every line points to a real, checkable rule.

AI Advocates But Never Decides, The Guardrail Flow

AI Advocates But Never Decides, The Guardrail Flow

And critically: if the AI can't find a real exemption that applies, it says so plainly. It does not invent one. No exemption means no brief means the content goes through normal review like it should. The system fails toward caution, not toward fabrication.

This is the interesting contrast with another build I've written about. In that case I designed an AI intake agent that's forbidden from quoting a number. There, the right move was to constrain the AI from doing something it shouldn't.

Here, the right move was to arm a human to do something they should. Two opposite tactics, same underlying philosophy: put the model in service of the expert's judgment, never in place of it. Sometimes that means tying the AI's hands. Sometimes it means handing your expert a better weapon. The skill is knowing which situation you're in.

The Result: A Faster Content Cadence, Same Compliance Standard

The back-and-forth that was killing the firm's content cadence got shorter.

The advisor walked into review with the exemption citation already in hand. Conversations that used to take multiple rounds collapsed into one. Instead of "I'm not sure about this, revise it," the reviewer got a specific rule, verbatim, with a one-line explanation. There was nothing left to argue about because the case was already made.

Let me be honest about what didn't change, because this is the part that matters most.

The compliance standard stayed exactly the same. Nothing non-compliant got through. The violation auditor was still running, still catching genuine problems, still doing its job. I did not lower the bar by a single inch.

The only thing that changed was that compliant content stopped getting wrongly killed. The good stuff that was dying in review now survived, because the advisor could prove it was good.

That distinction is the entire point. I didn't make compliance looser. I made it more accurate. The firm's standard for what's allowed didn't move; the friction around proving what's allowed dropped sharply.

That's what compliance friction reduction actually looks like in practice. Not cutting corners, not pushing risky content through, just removing the tax that over-caution quietly charges on every legitimate piece. If you want the broader version of how I approach this, I've written the full shipping AI content in a regulated industry playbook.

Where This Pattern Applies in Your Firm

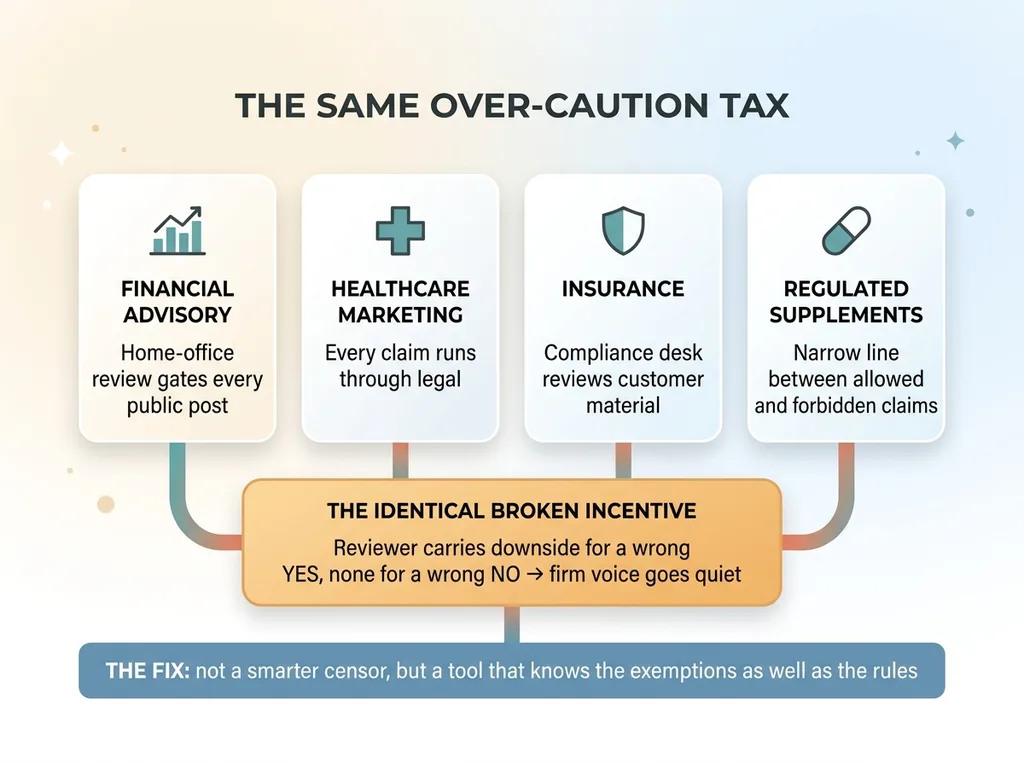

This isn't specific to financial advisory. Any regulated firm where a central reviewer gates communications has the exact same over-caution tax.

Where the Over-Caution Tax Applies Across Industries

Where the Over-Caution Tax Applies Across Industries

Healthcare marketing where every claim runs through legal. Insurance where a compliance desk reviews customer-facing material. Law firms with their own approval bottlenecks. Regulated supplements, where the line between an allowed claim and a forbidden one is narrow and the reviewer defaults to killing anything close.

In every one of those, the broken incentive is identical. The reviewer carries the downside for a wrong yes and none for a wrong no. So they say no, and your firm's voice goes quiet while less cautious competitors publish freely.

The fix is never a smarter censor. You already have caution covered. The fix is a tool that knows the exemptions as well as it knows the rules, and hands your experts a defensible, cited case for the content that should ship.

I'll be straight about what this takes. It requires your actual rulebook and real domain knowledge to do safely. A generic prompt will hallucinate rule numbers and torch your credibility the first time someone checks. This only works grounded against your real regulatory source material, built for your specific framework.

If compliance friction is quietly capping how much your firm can say in public, that's a solvable problem. But I won't recommend anything before I see where the bottleneck actually lives. Tell me where compliance is killing your content cadence and I'll take a real look.

Want to explore what AI could do for your business?

Book a free 30-minute strategy call. No pitch deck, no sales team, just a real conversation about your operations and where AI actually fits.

Get AI insights for business leaders

Practical AI strategy from someone who built the systems — not just studied them. No spam, no fluff.

Hodgen.AI

Ready to automate your growth?

Book a free 30-minute strategy call with Hodgen.AI.

Book a Strategy Call