FINRA Compliant Google Ads: How I Run Paid Search

How I built a system for FINRA compliant Google Ads that bans prohibited terms, uses an exemption, and pushes disclosures to the landing page where they belong.

By Mike Hodgen

The Problem: Half the Words That Convert Are Banned

I had a financial advisory firm come to me with a problem that sounds simple and isn't. They wanted to run FINRA compliant Google Ads, and they couldn't. Not because they didn't have budget. Not because they didn't understand paid search. Because every word that actually converts in a search ad was banned by their broker-dealer's advertising manual.

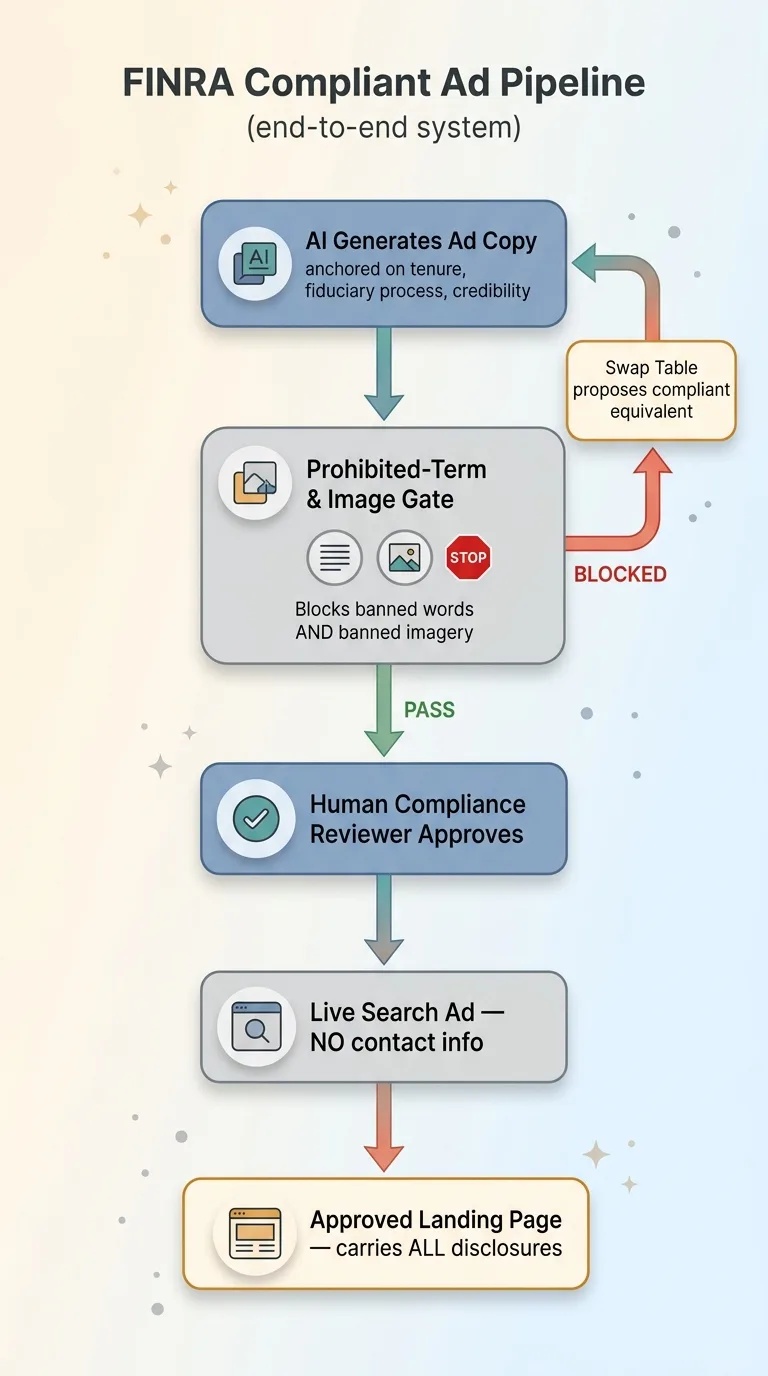

The FINRA Compliant Ad Pipeline (end-to-end system)

The FINRA Compliant Ad Pipeline (end-to-end system)

Think about the language a normal Google Ads template leans on. "Guaranteed returns." "Best financial advisor in town." "Maximize your wealth." "Top-performing portfolios." Upward-arrow imagery on the landing page. Promissory phrasing that implies you'll definitely make money.

Every single one of those trips a rule. FINRA prohibits promissory language, performance guarantees, exaggerated claims, and unwarranted superlatives. The broker-dealer's own manual usually goes further than FINRA does, because the broker-dealer is the one who eats the fine.

So here's the trap. Generic Google Ads advice is useless in a regulated industry, because every high-converting template the agencies hand you is built on language you're not allowed to use. You hire a paid search agency, they run their playbook, and either they ship something non-compliant (regulatory risk) or they look at the rulebook, get scared, and quietly refuse to touch the channel (lost growth).

Let me answer the doubt directly, because it's the one every regulated firm has. Yes, you can run paid ads in a regulated industry. You just can't do it the way the agency playbooks tell you to.

The fix isn't "be more careful with your copy." Careful copy fails the moment you're busy. The fix is structural. You change where the disclosures live, you build a gate that physically can't publish a banned term, and you rewrite toward language that's compliant and still persuasive.

That's what I built for this firm. Here's how it works.

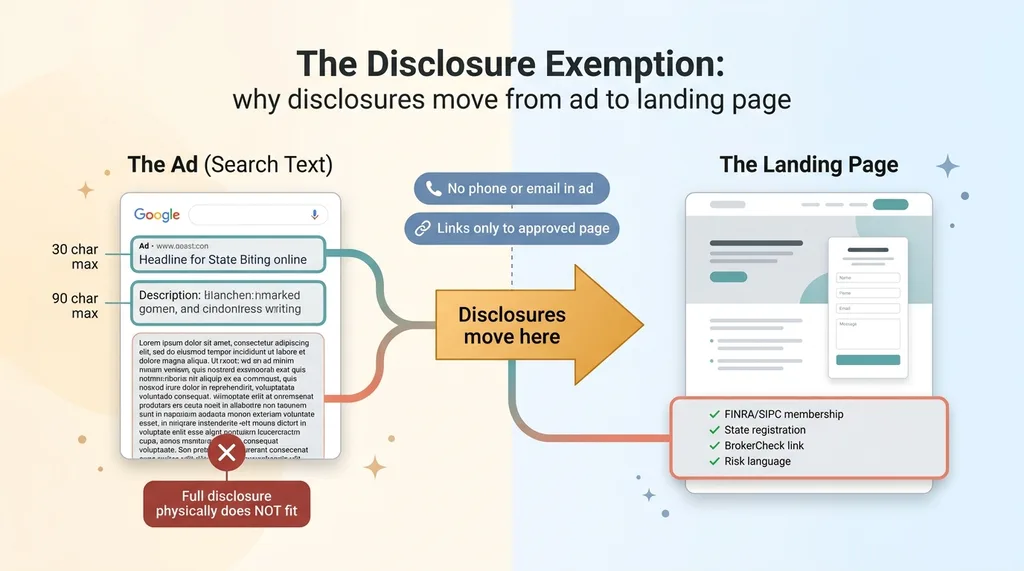

The Disclosure Exemption Most Firms Don't Know Exists

The thing that unlocked the entire project was a structural insight about disclosures, and most firms I talk to don't know it exists.

Why the full disclosure can't live in the ad

A standard compliant financial services ad carries a fat legal disclosure. FINRA/SIPC membership statement. State registration language. A reference to BrokerCheck. Required risk language depending on what you're advertising.

That disclosure does not fit in a Google text ad. It physically cannot. You have headlines capped at 30 characters and descriptions capped at 90. There is no version of "Securities offered through [BD], member FINRA/SIPC. Registered in CA, TX, AZ. Check BrokerCheck for background." that fits in a paid search ad. It's not even close.

So firms conclude they can't run paid search at all. The disclosure won't fit, so the channel is off the table.

The condition that makes the exemption work

Here's what changes the math. Search text ads generally don't require the full disclosure in the ad itself, provided two conditions hold: the ad contains no phone number or email address, and it links to an approved landing page that carries the disclosures.

The Disclosure Exemption: why disclosures move from ad to landing page

The Disclosure Exemption: why disclosures move from ad to landing page

Read that again, because it's the whole game. No contact information in the ad. Approved destination only. The required disclosures move off the ad and onto the page where they belong, and the ad becomes a compliant pointer to a compliant destination.

That's a structural decision, not a copywriting trick. We made a hard rule: zero contact info in any search ad, and the only allowed destination is the firm's approved, disclosure-bearing landing page. Once that rule is in place, the ad copy is freed from carrying the legal load it could never carry anyway.

Two honest caveats. First, this is general practice, not legal advice. Every firm has to confirm this against its own broker-dealer's advertising manual, because the BD's rules are often stricter than FINRA's baseline and the BD is the one approving your ads. Second, this exemption applies to search text ads. It does not automatically extend to every format. Display, video, and social have their own rules. Don't assume the search logic carries over.

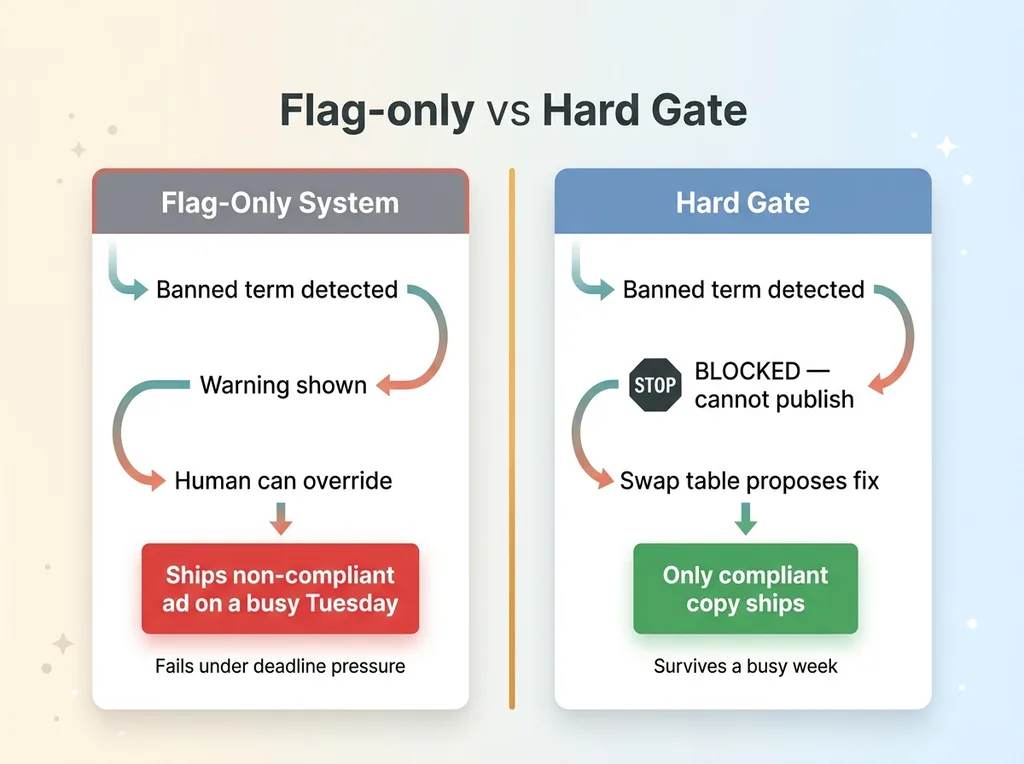

The Prohibited-Term-and-Image Gate

With the disclosure problem solved structurally, the next risk is the copy itself. And here's where most compliance setups quietly fail.

Banned terms, banned outright

Before any ad copy is approved, it runs against a list of prohibited terms and phrasing patterns. Superlatives like "best" and "top." Promissory language like "guaranteed" and "will grow." Performance guarantees. Exaggerated claims. Comparison language that implies you outperform competitors you can't legally name.

Flag-only vs Hard Gate comparison

Flag-only vs Hard Gate comparison

Anything that matches gets blocked. Not flagged and shipped. Blocked.

That distinction is the whole point. I've watched flag-only systems fail in real companies, including mine. A flag-only system shows a warning and lets a human decide. Sounds reasonable. But on a busy Tuesday with a deadline, someone overrides the flag because they're sure it's fine, and now you've shipped "maximize your returns" into a live FINRA-regulated ad.

A hard gate that refuses to publish is the only version that survives a busy week. I wrote about why nothing ships until it passes compliance because this is the single most important design choice in regulated content. The gate doesn't ask permission. It blocks.

Why images need the same gate

The same logic applies to imagery, and firms forget this constantly. Upward-arrow growth charts imply guaranteed returns. Dollar-sign motifs imply wealth outcomes you can't promise. Stock photos of yachts and mansions imply a lifestyle guarantee.

So images run the same gate. Anything that visually implies guaranteed returns or exaggerated outcomes gets blocked before it reaches a landing page or display unit. This is part of the broader regulated-content playbook I run across every client in a regulated vertical.

One honest limitation: the gate produces false positives. It occasionally blocks legitimate copy because a word matched a pattern in a context that was actually fine. That's a feature, not a bug, but it means you need a recovery path. That recovery path is the swap table, which is the next section.

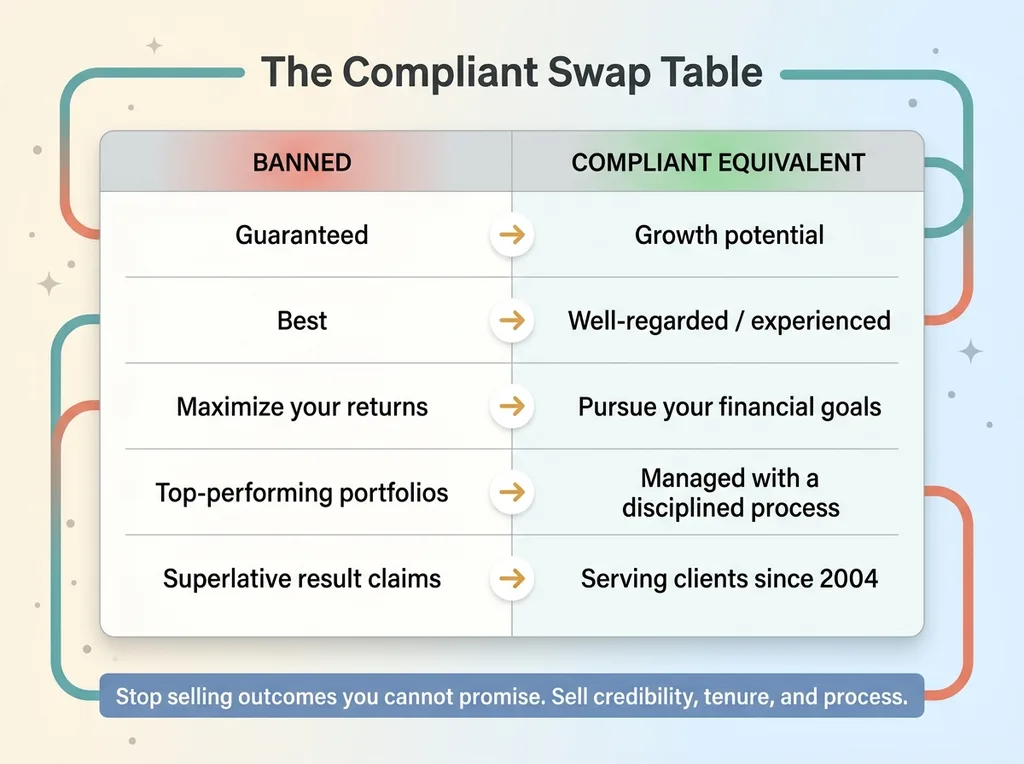

The Compliant-Copy Generator and the Swap Table

This is the practical heart of the system, because blocking banned words is easy. Keeping the ad persuasive after you strip them is the hard part.

From banned phrase to compliant equivalent

When the gate blocks a term, it doesn't just delete it. It proposes a compliant equivalent from a swap table. Here are anonymized real examples from what we built:

The Swap Table: banned phrase to compliant equivalent

The Swap Table: banned phrase to compliant equivalent

- "Guaranteed" becomes "growth potential"

- "Best" becomes "well-regarded" or "experienced"

- "Maximize your returns" becomes "pursue your financial goals"

- "Top-performing portfolios" becomes "managed with a disciplined process"

- Superlative claims about results become experience-and-tenure framing: "serving clients for years"

Notice the pattern. We stopped selling outcomes the firm couldn't promise, and started selling things the firm could actually stand behind: credibility, tenure, fiduciary process, suitability.

Generating copy that still converts

The generator doesn't just strip and swap. It rewrites the whole ad toward a different anchor. Instead of "we'll grow your money," the copy anchors on "we're a fiduciary, we've done this for two decades, here's our process."

Here's the lesson that surprised the firm. Compliant copy isn't weaker copy. It's differently anchored copy. The outcome-promise ads they wanted to run are the ones their target client has learned to distrust, because every scammy advisor runs them. Trust-and-process framing actually converts better with a sophisticated buyer who's choosing where to put serious money.

One discipline I never break: the generator proposes, a human compliance reviewer approves. The AI does the heavy lifting, drafts the compliant version, runs the gate, and hands a clean candidate to a human. The human still signs off before anything goes live. That human-in-the-loop step is non-negotiable in a regulated industry, and it's a lot faster to approve a pre-cleaned candidate than to write from scratch.

Where the Disclosures Actually Live: The Landing Page

Because the ad carries no disclosure burden under the exemption, the landing page carries all of it. Every bit.

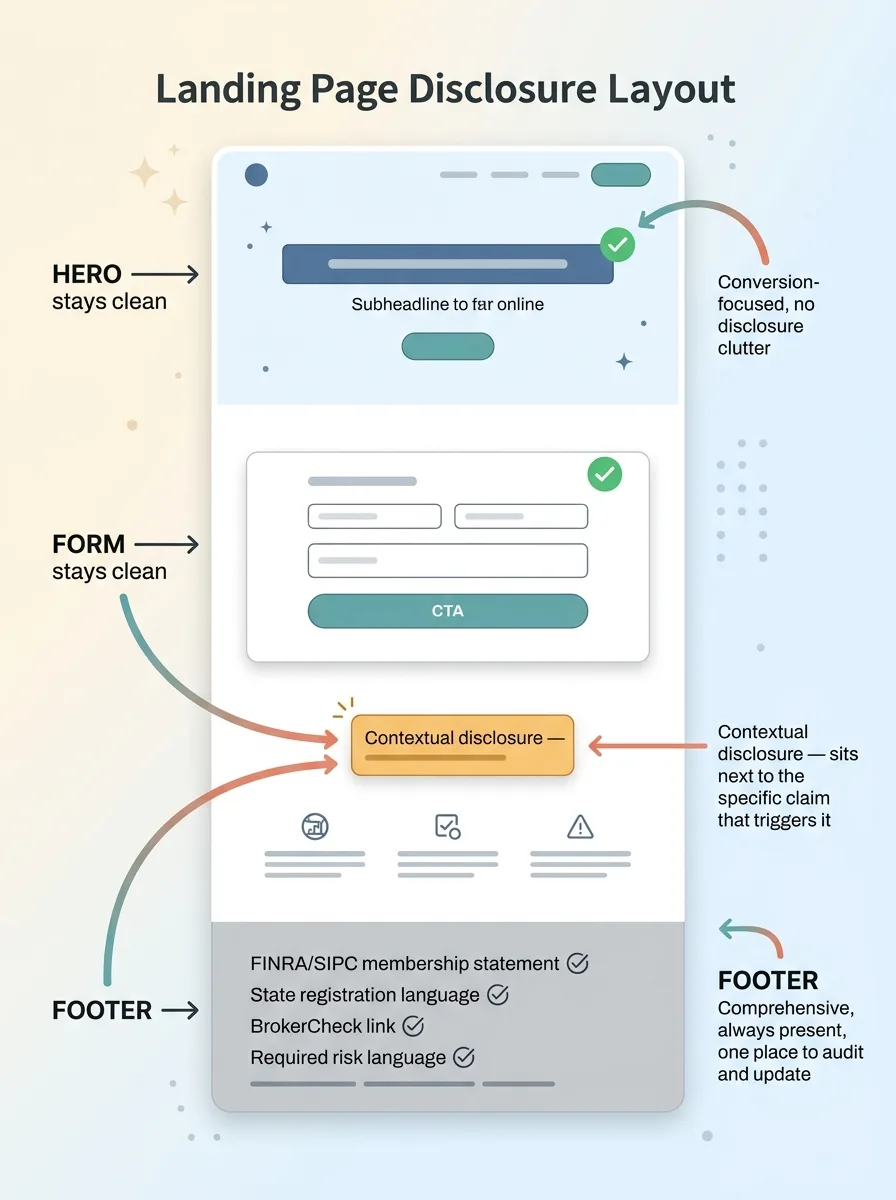

Landing page disclosure layout (clean conversion vs disclosures)

Landing page disclosure layout (clean conversion vs disclosures)

That means the FINRA/SIPC membership statement, the state-registration language, the BrokerCheck link, and any required risk language all live on the page the ad points to. This is non-negotiable, because the exemption only holds if the destination actually carries the disclosures. No disclosures on the page, no exemption, and now your "compliant" ad isn't compliant at all.

The design tension is real. The disclosures have to be present and accessible, but they can't crush conversion. Nobody fills out a contact form if the page reads like a legal brief.

The way I handle it: a clean, conversion-focused page body with the disclosures in the footer, plus contextual disclosure where a specific claim needs it. The footer is comprehensive and always present. The contextual disclosures sit next to the specific statements that trigger them. The hero and the form stay clean.

Two more requirements. The destination has to be on the firm's approved site, not a random campaign microsite the BD never reviewed. And the ad-to-page message match has to stay tight, both because Google's quality score depends on it and because a mismatch between ad and page is itself a compliance problem.

There's a quiet benefit here too. Putting every disclosure in one controlled place keeps the firm honest and makes audits trivial. When a state registration changes or a BD requirement updates, you change it in one place. No hunting through dozens of ad variations to find where the old language is hiding.

Why This Beats Hiring an Agency That Doesn't Know the Rules

Here's the cost-and-risk argument, plainly.

A general paid search agency gives you one of two bad outcomes. Either they run their standard playbook and ship non-compliant ads, which is regulatory risk that lands on the broker-dealer and the firm. Or they read the rulebook, decide it's too dangerous, and refuse to touch paid search at all, which is lost growth in a channel your competitors are using.

Neither is acceptable. The whole problem is that compliance and conversion pull in opposite directions, and a general agency isn't built to hold both.

The system solves it by encoding the rules once. Every ad is compliant by construction, not by hoping the next freelancer remembers the manual. The exemption is applied correctly every time. The gate can't ship a prohibited term. The swap table keeps the copy converting. The disclosures sit on the approved page.

Let me be honest about the win, because I won't inflate it. This firm didn't go from a mediocre paid channel to a great one. They went from being unable to safely run paid search at all to running it. That's the difference between zero paid pipeline and a working channel. For a firm that had sat out of paid search entirely because of compliance fear, that's the whole ballgame.

This pattern repeats across regulated verticals. I've built the same kind of compliance gating in other ad formats too, including an AI that audits radio ads in 60 seconds for spoken-word spots where the rules are just as strict and the review used to take a day. Encode the rules once, apply them everywhere, ship safely.

If You're a Regulated Firm Sitting Out of Paid Search

Here's the fear I hear most: that you have to choose between growth and compliance. That if you want to run ads, you have to risk a violation, and if you want to stay clean, you have to stay off the channel.

You don't have to choose. The constraint is real, but it's an engineering problem, not a reason to stay off paid search.

A system like this gives you four things. The disclosure exemption applied correctly, so your ads aren't carrying a legal load they can't hold. A hard gate that physically can't ship a prohibited term, even on your busiest week. A swap table that keeps your conversion intact while staying inside the rules. And disclosures parked on the approved landing page where they belong, in one place you can audit and update.

If your broker-dealer's advertising manual is the reason you've never run a paid ad, that's exactly the kind of constraint I encode into a working system. The rulebook isn't the obstacle. Not having the rulebook built into your tooling is the obstacle. Talk to me about your ad compliance setup and I'll tell you straight whether this fits your situation.

Ready to bring AI leadership into your company?

I work with a small number of companies at a time. If you're serious about AI, apply to work together and I'll review your application personally.

Get AI insights for business leaders

Practical AI strategy from someone who built the systems — not just studied them. No spam, no fluff.

Hodgen.AI

Ready to automate your growth?

Book a free 30-minute strategy call with Hodgen.AI.

Book a Strategy Call